- Why crypto tax in India is different from stock tax

- The flat 30% rule explained

- The 1% TDS rule explained

- Losses — the harsh truth every trader must know

- Which crypto transactions are taxable?

- How to calculate your tax (step by step)

- Filing your ITR — the right way

- Common tax mistakes that cost money

- Frequently asked questions

Why crypto tax in India is different from stock tax

If you are an Indian crypto trader, you need to understand something important from the start. Crypto tax in India is much harsher than tax on stocks or mutual funds.

When you sell stocks in India, you pay short-term capital gains (15%) or long-term capital gains (10% after ₹1 lakh exemption) depending on holding period. You can offset losses from one stock against profits from another. You can carry forward losses to future years.

Crypto has none of these benefits. Instead, India introduced a special tax for crypto (officially called "Virtual Digital Assets" or VDA) in the 2022 budget. The rules are simple — simple in a way that mostly favours the government, not the trader.

The three hard facts of Indian crypto tax:

- Flat 30% tax on all crypto profits, regardless of holding period or income bracket.

- 1% TDS (tax deducted at source) on every crypto sale, automatically deducted by the exchange.

- Losses cannot be offset against other crypto profits, stock profits, or any income. Losses cannot be carried forward either.

These three rules mean Indian crypto traders face one of the harshest tax regimes in the world. Even professional traders who make consistent profits find their effective returns significantly reduced by taxation.

A quick example:

Say you buy Bitcoin for ₹1 lakh and sell 6 months later for ₹1.5 lakh. Profit: ₹50,000. Your tax bill: ₹15,000 (30%) + ₹600 (4% cess on the tax) = ₹15,600. Plus the 1% TDS that was already deducted (₹1,500 on a ₹1.5 lakh sale). Effective tax rate on your ₹50,000 profit: 31.2% — before cess is added.

Now imagine you had a loss of ₹30,000 on a different coin in the same year. In stocks, this loss would reduce your ₹50,000 profit to ₹20,000 taxable. In crypto, no — you still pay full tax on the ₹50,000 profit, and the ₹30,000 loss is completely wasted. No offset. No carry-forward.

This is why many professional traders have reduced their Indian crypto trading activity since 2022, or moved to P2P and international platforms (which has its own legal risks). For retail traders, understanding the tax rules is essential to making net profits that are actually profitable after tax.

This guide walks through every rule clearly, with examples in simple English. By the end, you will know exactly what you owe, how to calculate it, and how to file correctly.

The flat 30% rule explained

The central rule of Indian crypto tax is Section 115BBH of the Income Tax Act, introduced in Budget 2022. It says:

Any income from transfer of Virtual Digital Assets (VDAs) shall be taxed at a flat 30%, plus applicable cess and surcharge.

The core rule — 30% flat tax plus 4% cess, regardless of holding period or total income.

What this means in plain English:

- Every rupee of profit from crypto is taxed at 30%.

- This is the same rate whether you hold for 1 day or 10 years. No "long-term" benefit.

- This is the same whether your total income is ₹5 lakh or ₹5 crore. No slab benefit.

- A 4% health and education cess is added on top of the tax amount. So effective rate becomes 31.2%.

- For very high-income individuals, additional surcharge applies (2-3% more).

What qualifies as a VDA?

Section 2(47A) defines VDA broadly. It includes:

- Bitcoin, Ethereum, and all other cryptocurrencies.

- Stablecoins like USDT and USDC.

- Non-fungible tokens (NFTs).

- Any digital asset that is generated through cryptographic means (with some exceptions).

Basically, anything you would call "crypto" is a VDA under this law.

What is NOT deductible against crypto profits:

Here is where it gets painful. Section 115BBH specifically says:

- No deduction is allowed for any expense other than the cost of acquisition.

- No deduction for trading fees, exchange fees, internet bills, laptop, or any other cost.

- No deduction for interest if you borrowed money to buy crypto.

- No deduction for research tools, data subscriptions, or educational courses.

The only thing you can subtract from your sale price is the cost of buying that specific crypto. Everything else is your expense to bear, with no tax benefit.

Example:

You buy 1 BTC for ₹50 lakh. You pay ₹5,000 in exchange fees on the buy. Total you paid: ₹50,05,000.

Six months later, you sell it for ₹60 lakh. You pay ₹6,000 in exchange fees on the sell. You receive net: ₹59,94,000.

How tax is calculated:

- Sale price: ₹60 lakh (not ₹59,94,000 — the fees cannot be deducted).

- Cost of acquisition: ₹50 lakh (not ₹50,05,000 — the buy fees also cannot be deducted).

- Taxable profit: ₹10 lakh.

- Tax at 30%: ₹3,00,000.

- 4% cess on tax: ₹12,000.

- Total tax owed: ₹3,12,000.

Your actual profit after real fees (₹11,000 in trading fees): ₹9,89,000. After the ₹3,12,000 tax, you net ₹6,77,000 — about 67.7% of your gross profit. Roughly 32% goes to the government through tax and fees.

This is painful but must be factored into all your trading decisions. A trade that looks like a ₹1 lakh profit is really only ₹65-68 thousand in your pocket.

The 1% TDS rule explained

Beyond the 30% tax, India also introduced a 1% Tax Deducted at Source (TDS) on crypto transactions under Section 194S, which came into effect from July 1, 2022.

The 1% TDS flow — automatically deducted by the exchange on every crypto sale.

What TDS means in simple words:

TDS is a tax the government collects at the moment of a transaction, not at the end of the year. When you sell crypto on an Indian exchange, the exchange automatically takes 1% of the sale value and sends it to the government. You only receive the remaining 99%.

Think of it like GST. When you buy a product from a shop, the shop collects GST and sends it to the government — you do not pay it separately at year-end. TDS works the same way — except it is your money being held, and you can claim it back in your ITR.

A simple example:

You sell 1 BTC for ₹60 lakh on an Indian exchange.

- Sale value: ₹60,00,000.

- 1% TDS deducted by exchange: ₹60,000.

- You receive in your account: ₹59,40,000.

- The ₹60,000 goes to the Income Tax Department in your PAN.

This ₹60,000 is not the full tax you owe. It is just an advance deposit. When you file your ITR at year-end, you calculate your actual 30% tax on profits, and the TDS is subtracted from that final bill. If TDS is higher than your actual tax, you get a refund. If your tax is higher, you pay the difference.

Key points about TDS:

1. TDS applies on the sale value, not just the profit. You pay 1% even if you are selling at a loss. This is particularly painful for traders who make many small trades — TDS keeps taking money even when you are losing.

2. TDS applies to both crypto-to-INR and crypto-to-crypto swaps. When you swap USDT for BTC, TDS applies. When you sell BTC back to INR, TDS applies again. Every transaction that transfers a VDA creates a TDS event.

3. Threshold limits exist. TDS applies to sales above ₹10,000 per transaction for most individuals. For "specified persons" (certain businesses), the threshold is ₹50,000. Small trades below these limits do not trigger TDS.

4. Indian exchanges do this automatically. You do not need to calculate or pay TDS manually. The exchange handles it.

5. On foreign exchanges, you are responsible. If you trade on a foreign exchange (not registered in India), the exchange will not deduct TDS. You are legally required to deduct and pay it yourself — which is practically impossible for retail traders. This is one reason many Indian users avoid foreign exchanges despite often better features.

Why TDS was introduced:

The government's goal was to create a paper trail of every crypto transaction. Before TDS, crypto trades were hard to track. With TDS at 1%, every trade is now reported to the government in real time. Even if you do not file your ITR properly, the government has a record of your activity.

The practical impact:

Heavy traders — especially day traders and scalpers — suffer the most from TDS. Each trade costs them 1% even if it was a small winning trade. Over hundreds of trades, TDS drains significant capital. This is why frequent crypto trading in India has become much less profitable since 2022. Long-term investors who trade rarely are much less affected.

Losses — the harsh truth every trader must know

This is the single most painful rule in Indian crypto tax. You must understand it clearly before you trade.

Rule: Losses from crypto cannot be set off against anything. They are effectively wasted.

Let me explain what this means with four examples.

Example 1 — Loss on one coin cannot offset profit on another.

In a single year:

- You made ₹2 lakh profit on Bitcoin.

- You made ₹1 lakh loss on Dogecoin.

In stocks, your net taxable gain would be ₹1 lakh (₹2L profit minus ₹1L loss). In crypto — NO. You pay tax on the full ₹2 lakh Bitcoin profit. The ₹1 lakh Dogecoin loss is completely wasted. Tax owed: ₹2L × 31.2% = ₹62,400.

Example 2 — Crypto losses cannot offset stock or mutual fund profits.

You lose ₹5 lakh on crypto this year. You also make ₹5 lakh profit on your stock portfolio. In many countries, these would offset. In India — they do not. You pay tax on the full ₹5 lakh stock profit. The ₹5 lakh crypto loss is simply gone.

Example 3 — Crypto losses cannot be carried forward.

In stocks, if you have a ₹10 lakh loss this year, you can carry it forward up to 8 years and offset it against future profits. In crypto — NO. A loss in FY 2025-26 is wasted forever. Even if you make ₹10 lakh profit in FY 2026-27, you pay full tax on that future profit. The prior loss does not help you.

Example 4 — Losses from one type of VDA cannot offset gains from another.

This is actually disputed. Some tax experts argue that within the same financial year, losses from one crypto can be set off against gains from another crypto (because Section 115BBH talks about gains from "transfer of VDA" as a category). Others interpret strictly — each trade is its own taxable event.

Most practitioners take the middle position: losses from crypto X and gains from crypto Y in the same year can be netted for tax purposes, but losses cannot go beyond zero (you cannot reduce other-category income, and cannot carry forward).

What this means practically for your strategy:

Strategy shift 1 — Avoid too many small speculative bets. Since losses are wasted, the cost of failed bets is very high. You pay the full loss, and you get no tax benefit. Concentrating on fewer, higher-conviction positions makes more tax sense than many small gambles.

Strategy shift 2 — Prefer long-term holding over active trading. Each active trade creates a taxable event (and 1% TDS). Long-term holding has fewer taxable events. Since there is no long-term capital gains benefit, this is about minimising events, not reducing rates.

Strategy shift 3 — Be realistic about tax on profits. When calculating your returns, always subtract the 31.2% tax. An 8% monthly trading profit is only 5.5% after tax. Many trading strategies that look profitable on paper actually lose money after tax.

Strategy shift 4 — Keep detailed records. Without records, you cannot even calculate your net position correctly. Track every buy, every sell, every swap, every fee, with dates and values in INR. This is essential both for ITR filing and for your own performance analysis.

The tax structure heavily favours buy-and-hold investors over active traders. For most Indian retail participants, a dollar-cost averaging strategy on top-tier coins minimises taxable events while still allowing wealth building.

Which crypto transactions are taxable?

Not every crypto activity creates a taxable event. But many do. Here is the complete list.

Taxable events (create a 30% tax liability):

1. Selling crypto for INR. Obvious one. You sell BTC for rupees, profit is taxable. Both 30% tax and 1% TDS apply.

2. Swapping one crypto for another. You swap 1 ETH for BTC. This is considered two transactions — selling ETH for the BTC's equivalent INR value, then buying BTC. Profit/loss on the ETH side is taxable. 1% TDS applies.

3. Using crypto to buy goods or services. You use BTC to buy something from an online store. Technically you sold the BTC at its market value and bought the item. Profit on BTC sale is taxable.

4. Receiving crypto as income. If you receive crypto as payment for work, consulting, or services, it is treated as income at the market value on the date received. Plus when you eventually sell it, the profit above that value is taxable again under VDA rules.

5. Receiving crypto as gifts. Crypto gifts exceeding ₹50,000 in total per year are taxable as income. (This is outside the 30% VDA rule — it is taxed as "income from other sources" at your slab rate.)

6. Earning from staking, mining, yield farming. Rewards received from staking or DeFi yield are taxable as income at market value when received. Then subsequent sales trigger VDA tax again.

7. Airdrops. Tokens received through airdrops are taxable at market value when received.

Events that are generally NOT taxable:

1. Buying crypto with INR. No tax event. You are simply exchanging cash for an asset.

2. Moving crypto between your own wallets. Not a taxable event. This is just moving your property around.

3. Holding crypto. Simply holding does not create tax. You are not taxed on unrealised gains.

4. Receiving crypto from yourself. If you transfer crypto from one of your wallets to another, no tax.

Grey area — DeFi activities:

DeFi activities are less clear. Lending, borrowing, providing liquidity, and yield farming involve complex on-chain events. Practitioners generally treat:

- Depositing into a DeFi protocol: NOT taxable (considered a transfer, not sale).

- Receiving rewards/yield: Taxable as income at time of receipt.

- Converting LP tokens back to underlying assets: May be taxable if value has changed.

Our DeFi guide covers the mechanics of these activities — but for tax purposes, always consult a CA familiar with crypto when doing significant DeFi activity.

A practical takeaway:

Active trading creates many taxable events. Long-term holding creates few. This is another reason the Indian tax structure favours patient, low-frequency investors. If your strategy involves hundreds of trades per year, each one is a separate tax calculation — a record-keeping burden most retail traders underestimate.

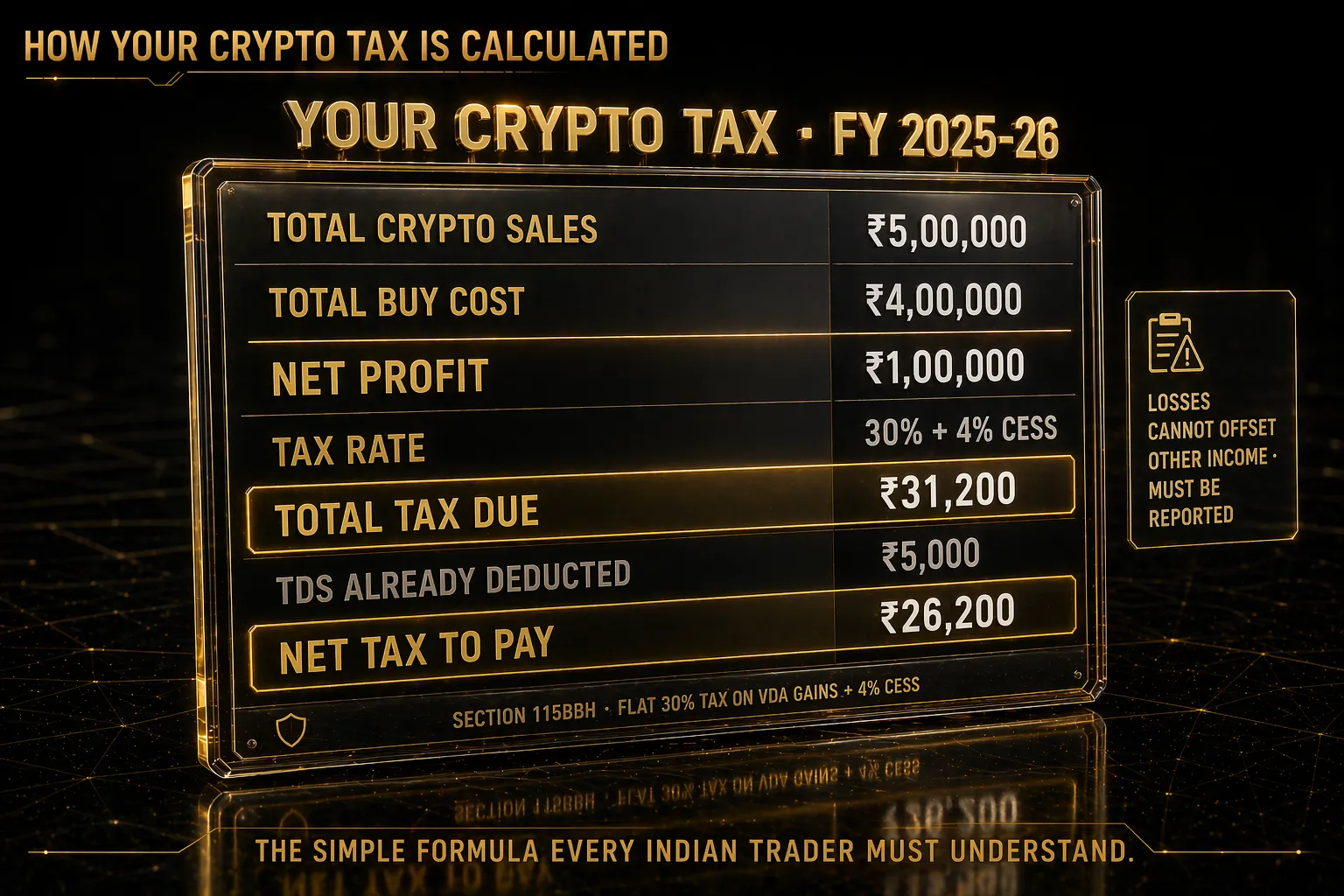

How to calculate your tax (step by step)

Let us walk through a full tax calculation for a typical Indian crypto trader. This is practical — follow along with your own numbers.

A complete crypto tax calculation — every row you need to fill in to know your actual tax bill.

Step 1 — Gather all transaction data for the financial year.

Download transaction history from every exchange you used between 1 April and 31 March. Most Indian exchanges (CoinDCX, WazirX, others) provide CSV exports in their account settings. Include:

- Every buy transaction (date, coin, quantity, INR amount).

- Every sell transaction (date, coin, quantity, INR amount).

- Every swap (date, what was sold, what was bought, INR equivalent values).

- TDS deducted (should be in the exchange report).

Step 2 — Match buy and sell transactions (FIFO method).

For each coin, match sells against buys using FIFO — First In, First Out. The oldest coins you bought are treated as sold first. Example:

- Jan 2025: Bought 0.5 BTC for ₹30 lakh.

- Mar 2025: Bought 0.5 BTC for ₹35 lakh.

- Aug 2025: Sold 0.6 BTC for ₹42 lakh.

Under FIFO, the 0.6 BTC sold consisted of 0.5 BTC from January (cost ₹30L) and 0.1 BTC from March (cost ₹7L, being 0.1/0.5 × ₹35L). Total cost: ₹37L. Sale price: ₹42L. Profit: ₹5L.

Step 3 — Sum all profits and losses across coins.

Add up all your profits and losses for the year. Remember — losses on crypto cannot offset gains on other categories, but within crypto, there is some debate about inter-coin offsetting. Consult a CA for your specific case. For this example, assume you can offset within crypto:

- Profit on BTC trades: +₹5,00,000.

- Profit on ETH trades: +₹2,00,000.

- Loss on altcoin trades: -₹1,50,000.

- Net taxable crypto profit: ₹5,50,000.

Step 4 — Calculate base tax at 30%.

₹5,50,000 × 30% = ₹1,65,000.

Step 5 — Add 4% health and education cess.

₹1,65,000 × 4% = ₹6,600. Total tax: ₹1,71,600.

Step 6 — Add surcharge if total income is high.

If your total annual income exceeds ₹50 lakh, surcharge applies:

- ₹50L-1Cr: 10% surcharge on tax.

- ₹1Cr-2Cr: 15% surcharge.

- ₹2Cr-5Cr: 25% surcharge.

- Above ₹5Cr: 37% surcharge.

For most retail traders, no surcharge. For high earners, factor this in.

Step 7 — Subtract TDS already paid.

Your exchange reports should show total TDS deducted during the year. Say it was ₹80,000. Subtract from tax owed:

- Tax owed: ₹1,71,600.

- TDS already paid: ₹80,000.

- Net tax to pay with ITR: ₹91,600.

Step 8 — Pay advance tax if applicable.

If your tax liability exceeds ₹10,000 in a year, you are required to pay advance tax in four instalments during the year (June 15, Sep 15, Dec 15, Mar 15). Most traders miss this and end up paying interest penalties. For large crypto profits, check with a CA about advance tax obligations.

Step 9 — Save all records.

Keep every transaction CSV, every exchange statement, every screenshot of wallet transfers. Income Tax Department can audit up to 6-10 years back. Without records, you cannot defend yourself in an audit.

For most retail traders with under 100 transactions per year, manual calculation in Excel is manageable. For frequent traders, consider using crypto tax software like KoinX, ClearTax Crypto, or similar — they import from exchanges automatically and calculate FIFO-adjusted gains. Cost is typically ₹2,000-5,000 per year, a good investment for the time saved and reduced errors.

Filing your ITR — the right way

Having calculated your tax, you now need to file it correctly in your Income Tax Return (ITR). Here is how.

Which ITR form to use:

Most crypto-earning individuals use ITR-2 (if crypto is considered investment/capital gains) or ITR-3 (if crypto trading is your business). The distinction matters:

- ITR-2 — Capital gains route. For investors who hold crypto as investment. Crypto gains reported under "Income from VDA" with the 30% flat rate applied. This is the most common choice for retail traders.

- ITR-3 — Business income route. For traders whose crypto trading is substantial and intended as business. Crypto profits reported as business income. Some CAs recommend this for high-volume traders.

For most retail traders with fewer than 100 transactions per year and crypto as a side investment, ITR-2 under "Income from VDA" is appropriate.

Key schedules and sections to fill:

Schedule VDA (Virtual Digital Asset). This is the specific section for crypto. You report:

- Date of acquisition.

- Date of transfer (sale).

- Cost of acquisition.

- Consideration received (sale price).

- Income from transfer (profit).

If you have many transactions, you can use FIFO-based summary numbers rather than listing every single trade.

Schedule TDS-2. Where you report TDS deducted during the year, pulling from your Form 26AS and AIS statements.

Schedule AIS (Annual Information Statement). The Income Tax Department now receives data directly from Indian crypto exchanges. Your AIS will show your crypto trading activity. Make sure your ITR matches AIS — mismatches trigger notices.

Steps to file:

- Log in to incometax.gov.in.

- Download your Form 26AS and AIS — verify all crypto TDS and transactions.

- Calculate your taxes as shown in the previous section.

- Fill ITR-2 or ITR-3 online or use offline utility.

- Report crypto gains in Schedule VDA.

- Pay any balance tax before submission.

- Verify ITR via Aadhaar OTP or other methods.

- Keep acknowledgement and backup of all documents.

Deadlines to remember:

- ITR filing deadline (for most individuals): July 31 of the assessment year.

- Late filing deadline (with late fee): December 31.

- Advance tax instalments: June 15, Sep 15, Dec 15, Mar 15.

Missing deadlines triggers fees of ₹5,000-10,000 plus interest on unpaid tax. For large crypto profits, advance tax should be paid on time — interest under section 234B/C adds up quickly.

Should you use a CA or file yourself?

For simple cases (say, 5-20 trades, straightforward profit/loss), you can file yourself using the online ITR portal or tax software. Cost: free to ₹500.

For moderately complex cases (50-500 trades, swaps, some DeFi activity), a CA familiar with crypto can save you time and errors. Cost: ₹3,000-10,000.

For complex cases (hundreds of trades, international exchanges, staking rewards, NFT sales), definitely use a crypto-aware CA. Cost: ₹10,000-50,000 depending on complexity.

Not every CA understands crypto tax well. Ask specifically if they have experience with Section 115BBH and Schedule VDA. The extra effort to find a crypto-aware CA is worth it.

Common tax mistakes that cost money

Here are the mistakes Indian crypto traders make most often when filing taxes. Avoid all of them.

Mistake 1 — Not reporting crypto gains at all. Some traders assume the tax department does not know about their crypto. This was somewhat true before 2022. It is absolutely false now. Indian exchanges report to the tax department. Bank transfers linked to crypto purchases are tracked. Not reporting is now almost certain to be caught — with penalties that dwarf the original tax.

Mistake 2 — Not claiming TDS. TDS has already been deducted from your account. If you do not claim it in your ITR, you are double-paying tax. Always reconcile your TDS against your exchange reports and Form 26AS. This is unclaimed money belonging to you.

Mistake 3 — Treating losses as deductible. Some traders net crypto losses against stock gains or salary income. This is not allowed under current law (Section 115BBH). The ITR processing system will catch this and adjust the assessment, often with penalty interest.

Mistake 4 — Mixing crypto with other capital gains. Crypto has its own schedule (VDA). It is not mixed with stock capital gains. Report each separately. Confusing the two is a common filing error that delays processing.

Mistake 5 — Not keeping records. When you sell a coin you bought 3 years ago, you need to show the original cost. Without records, the tax department may assume the entire sale is profit (no cost to deduct). Keep all purchase records, preferably as CSV exports stored in cloud with backups.

Mistake 6 — Ignoring airdrop and staking income. Rewards received from staking, airdrops, and yield farming are taxable at market value when received. Many traders ignore these, then face notices when the AIS shows the income. Always report all crypto income, not just trading profits.

Mistake 7 — Using wrong valuation dates. For swaps, the INR value on the date of swap matters — not the original acquisition cost translated later. Use each day's actual INR equivalent from exchange records. Getting this wrong can result in over or under-reported profits.

Mistake 8 — Forgetting foreign exchange transactions. If you used a foreign exchange, you still owe tax in India. Not reporting foreign exchange activity is technically tax evasion, with serious consequences if discovered. If you have significant foreign exchange activity, definitely consult a CA.

Mistake 9 — Not paying advance tax. If your crypto profits are substantial, you need to pay advance tax during the year (not wait until filing). Interest under section 234B/C for unpaid advance tax can be 1-2% per month on the unpaid amount. For a ₹5 lakh tax bill, that can be ₹5,000-10,000 extra.

Mistake 10 — Assuming tax rules will not change. Indian crypto tax law is evolving. Budget 2024 and 2025 have made minor adjustments. Future budgets may bring more changes — possibly better, possibly worse. Stay updated. Follow trusted tax-focused crypto sources in India. Do not rely on outdated information.

VIDYA MANDAL — Know the rules before you play the game

VIDYA MANDAL is our structured knowledge library covering Indian crypto tax — the full rules, calculation examples, ITR filing walkthroughs, and the strategy adjustments every Indian trader should make in response to the current tax regime. If you are serious about net-of-tax profits, the knowledge here directly affects your bottom line.

Explore the Store →A final thought. Tax is the least exciting part of crypto. But ignoring it is the most expensive mistake a trader can make. The 30% + TDS + no-offset regime is harsh. But it is the reality of trading crypto in India right now. Build your strategy around it, keep detailed records, file correctly every year, and focus on long-term patient investing over active trading — that is how Indian crypto investors build wealth under this tax structure.

Before you start or scale your crypto trading, understanding how to buy legally and safely is also essential — our Indian Bitcoin buying guide covers the legal exchange landscape. For strategies that minimise taxable events, dollar-cost averaging is the most tax-efficient approach for most Indian retail investors.

Join our Telegram community where we share tax season tips and updates on any rule changes. Our crypto education courses include a full module on Indian crypto tax with calculation templates. Pay what you owe. Claim what is yours. Keep what remains. That is the path to sustainable crypto wealth in India.

Frequently asked questions

What is the current crypto tax rate in India for FY 2025-26?

Flat 30% on all crypto profits, plus 4% health and education cess (effective 31.2%), plus surcharge for high earners. This rate applies regardless of holding period — no distinction between short-term and long-term. Additionally, 1% TDS is deducted on every sale transaction by Indian exchanges automatically. No deductions are allowed except the cost of acquisition.

Can I offset my crypto losses against stock market gains in India?

No. Under Section 115BBH of the Income Tax Act, crypto losses cannot be offset against gains from any other category — not stocks, not mutual funds, not salary income, not business income. Crypto losses also cannot be carried forward to future years. They are effectively wasted for tax purposes. This is one of the harshest aspects of Indian crypto tax law.

How is the 1% TDS on crypto calculated and who deducts it?

1% TDS is calculated on the total sale value (not just the profit) of any crypto transaction above ₹10,000 for most individuals (₹50,000 for specified persons). Indian exchanges deduct it automatically when you sell. On a ₹10,000 sale, ₹100 is TDS, you receive ₹9,900. This TDS is an advance — you claim it back against your final tax liability when filing your ITR.

Do I have to pay tax on crypto-to-crypto swaps in India?

Yes. Every crypto-to-crypto swap is treated as two transactions — sale of the first crypto, and purchase of the second. Profit on the sale side is taxable at 30%. 1% TDS also applies to swap transactions on Indian exchanges. This makes active trading and portfolio rebalancing expensive — another reason the Indian tax structure favours long-term holding over frequent activity.

Which ITR form should I use to report crypto gains in India?

Most retail traders use ITR-2, reporting crypto under Schedule VDA (Virtual Digital Assets) with the 30% flat tax. Active traders whose crypto activity constitutes a business may use ITR-3 with business income treatment. ITR-1 (Sahaj) cannot be used if you have crypto gains. For complex situations with many trades, DeFi activity, or foreign exchanges, consulting a CA familiar with crypto tax is strongly recommended.

cRyPtO sMaRt is not registered with SEBI and does not provide investment advice. Crypto trading carries significant risk of capital loss. The strategies, examples, and opinions shared in this article are for educational purposes only. Always do your own research and consult a SEBI-registered financial advisor before investing real capital. Past performance does not guarantee future results.