- Why Indians compare crypto and stocks

- What are crypto and stocks, in plain English

- Ownership and rights — what you actually own

- Returns compared — the 10-year picture

- Volatility and risk — how much can you lose

- Tax and liquidity — the hidden costs

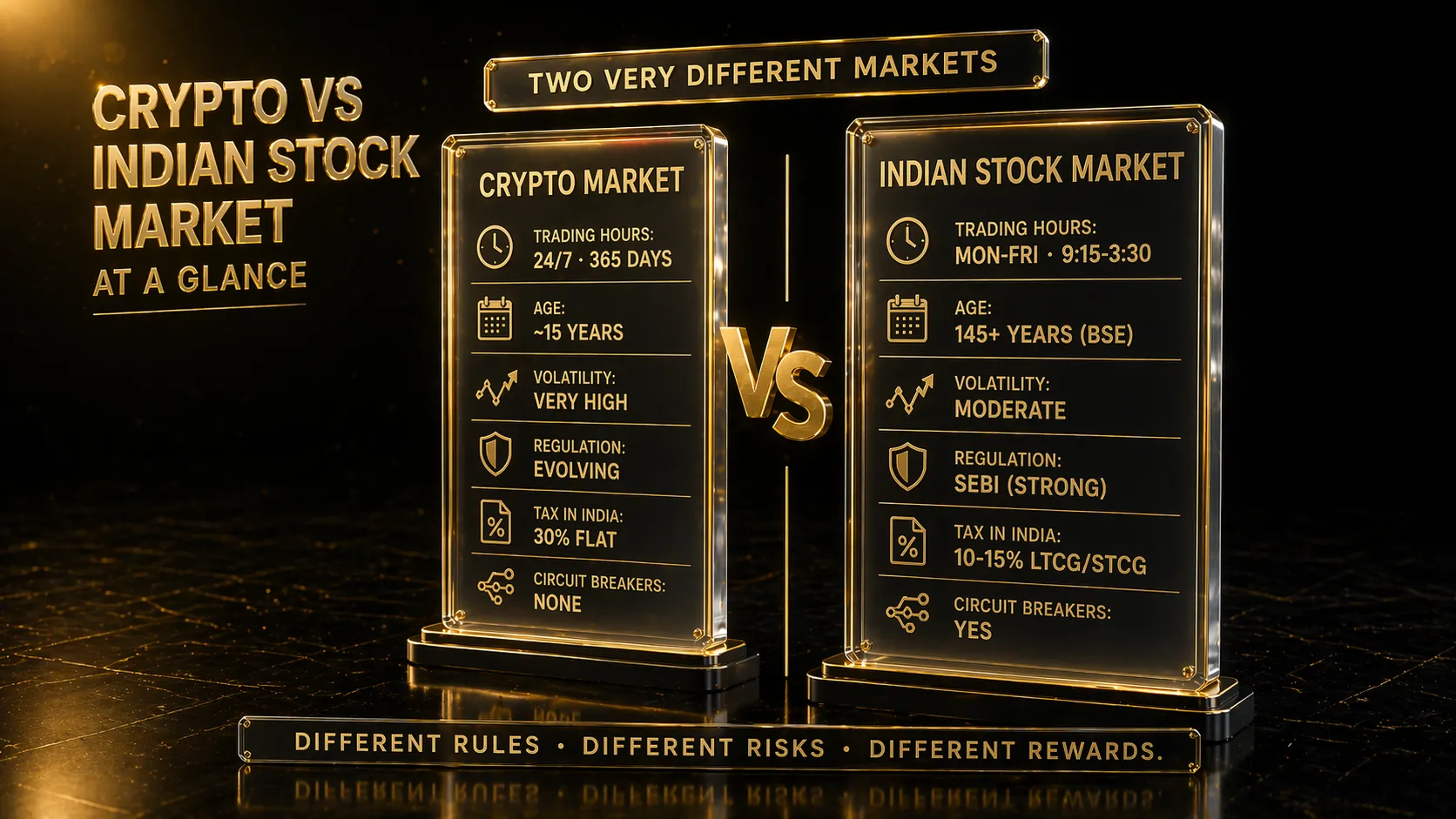

- Market hours and access — 24/7 vs 9:15-3:30

- How to combine both in one portfolio

- Frequently asked questions

Why Indians compare crypto and stocks

If you have ever thought about investing, you have probably asked this question — "should I put my money in crypto or in the stock market?" It is one of the most common questions from new Indian investors today.

The answer is not simple. Both are real ways to build wealth over time. But they work very differently. The rules are different. The risks are different. The tax treatment is different. And the kind of person each suits is different too.

Let me describe three typical Indian investors to make this real.

Investor A — Riya, 26, software engineer in Bengaluru. She earns ₹1 lakh per month. She invests ₹20,000 monthly. She has heard about crypto from her office friends. She is torn between starting a SIP in equity mutual funds and putting the money into Bitcoin. Which is right for her?

The honest answer — probably both, but in very different amounts. This guide will show her (and you) exactly how.

Investor B — Rahul, 35, owns a small business in Pune. He has ₹5 lakh in savings. He wants faster returns because he is behind on retirement planning. He is considering moving all ₹5 lakh to crypto altcoins because "everyone makes 10x in crypto".

The honest answer — this is a bad plan. He risks losing everything. Stocks have a role. Crypto has a role. No single asset takes 100% of a portfolio.

Investor C — Mrs. Sharma, 52, retired teacher in Kolkata. She has ₹30 lakh of life savings. She needs this money to be safe for retirement. Her nephew keeps saying crypto is the future and she should put 30% in.

The honest answer — at her age and situation, crypto should be 0-5% maximum. Stocks through good mutual funds and fixed income should be the bulk.

Different people need different mixes. This guide will not tell you which is "better". It will tell you how each works, when each fits, and how to combine both sensibly for your situation. By the end, you will make a much better decision than "pick one and hope".

What are crypto and stocks, in plain English

Before we compare, let me make sure you understand both clearly. No finance jargon. Plain language.

What is a stock?

When you buy a stock, you are buying a small piece of a real company. Say you buy 10 shares of Reliance Industries. You now own a tiny fraction of Reliance — its factories, its products, its profits, its future. If Reliance makes more profit and grows, your shares become worth more. If Reliance pays dividends (a share of profits), you get a cheque.

Stocks exist because businesses need money to grow. Instead of borrowing all the money from banks (which is expensive), companies sell shares to millions of people. Each person gets a piece of ownership.

In India, stocks trade on two main exchanges — BSE (Bombay Stock Exchange, the oldest in Asia, started 1875) and NSE (National Stock Exchange, started 1992). Regulators like SEBI make sure companies disclose proper information, follow rules, and do not cheat investors.

Over 150 years of history tells us stocks tend to grow about 10-12% per year on average in India — though individual years vary wildly. Quality Indian stocks have created massive wealth for patient investors over decades.

What is crypto?

Crypto is a type of digital asset that lives on a blockchain — a public, shared record book maintained by thousands of computers worldwide. Bitcoin was the first crypto, launched in 2009. There are thousands of cryptos now, each with different purposes.

Unlike stocks, most cryptos do not represent ownership of a company. Bitcoin represents nothing — it is simply a scarce digital token (only 21 million will ever exist). Ethereum represents access to a global computer that runs applications. Other coins represent governance rights, usage credits, or speculative bets on future technology.

Crypto has no central regulator. It is not issued by any country. It works 24 hours a day, 365 days a year, everywhere in the world. Anyone with internet can buy it.

Crypto is young — only about 17 years old. The long-term track record is short. Some cryptos have been amazing investments (Bitcoin grew from $0.001 to over $100,000). Many others have gone to zero. The volatility is extreme — 50-80% drops happen regularly.

The deepest difference.

Stocks are backed by real businesses producing real things (products, services, profits). If you buy HDFC Bank stock, there is a bank with branches, employees, customers, and revenue. Even if HDFC's stock price falls, the bank still exists and operates.

Crypto is backed by a network and code. Bitcoin's value depends on people agreeing it has value. If everyone suddenly stopped using Bitcoin, its price would go to zero — there is no underlying business. However, because Bitcoin has a scarcity property (only 21 million will ever exist) and is used globally as "digital gold", many investors treat it as a store of value similar to physical gold.

Neither is "better". They are different. Stocks benefit from company growth. Crypto benefits from network effects and adoption. Both can create wealth over time. Both can lose value. Both have their place in a diversified portfolio.

Ownership and rights — what you actually own

When you invest, what do you actually own? This matters more than most beginners realise. Because ownership determines your rights, protections, and what happens during problems.

Stock ownership in India — what you get:

- Fractional ownership of a registered company. The shares are held in your demat account, linked to your PAN.

- Voting rights at shareholder meetings (proportional to your holding).

- Dividend rights when the company decides to pay dividends from profits.

- Legal recourse if the company cheats you. SEBI, courts, and the Investor Education and Protection Fund exist to protect shareholders.

- Regulatory protection — companies must disclose financial results quarterly, follow accounting rules, and cannot just disappear without notice.

- Insurance of a sort through Investor Protection Funds (partial coverage in specific situations like broker default).

When you buy Tata Consultancy shares, you legally own part of Tata Consultancy. Even if your broker goes bankrupt, your shares remain yours (they are registered in your name in the depository).

Crypto ownership — what you really get:

- A private key — a long string of characters that gives you the right to spend certain coins. Whoever holds the private key controls the coins.

- No voting rights (except in specific governance tokens, and those rights are limited).

- No dividends (some coins offer "staking rewards", but these are not the same as company dividends).

- Limited legal recourse — if someone steals your coins, Indian police have limited tools to recover crypto (especially if it crosses borders). There is no SEBI for crypto yet.

- No regulatory protection currently. Indian law is evolving but most crypto operations fall outside traditional investor protection frameworks.

- No insurance for individual holdings. Some exchanges offer insurance on their own reserves, but your personal wallet is your own responsibility.

When you "buy" Bitcoin on an exchange, you often do not actually own the Bitcoin until you withdraw it to your own wallet. The exchange owns it and owes you an equivalent balance. If the exchange fails (FTX collapsed in 2022, costing users billions), you may lose everything — as FTX users learned the hard way.

This is a big difference.

With stocks, your ownership is recorded in a central database run by regulators. Even if your broker fails, your ownership is protected.

With crypto, your ownership depends on who controls the private keys. If you hold them yourself (self-custody in a hardware wallet), you have direct control. If an exchange holds them for you, you depend on the exchange's honesty and security.

The phrase "not your keys, not your coins" exists for this reason. If you take crypto seriously, you need to learn about self-custody. Our on-chain analysis guide explains the blockchain mechanics, but for security you should also consider a hardware wallet for long-term holdings.

For most beginners, this means: stocks are simpler and safer by default in India. Crypto requires learning additional security steps that are not needed for stock investing.

Returns compared — the 10-year picture

Now for the number everyone wants — what have these actually returned?

Two very different markets — different rules, different risks, different rewards.

Indian stock market — historical returns:

- Nifty 50 index (last 10 years): roughly 12-13% annualised (includes dividends).

- Sensex (last 20 years): roughly 13-14% annualised.

- Quality individual stocks (last 10 years): some, like Bajaj Finance or Asian Paints, delivered 20-25% annualised. But these are outliers.

- Equity mutual funds (last 10 years): well-managed funds returned 12-15% annualised on average.

Translation — ₹1 lakh invested in a Nifty 50 fund 10 years ago is worth about ₹3.3 lakh today. In quality stocks, it could be ₹7-10 lakh. This is real wealth building, at moderate risk, spread over time.

Crypto — historical returns:

- Bitcoin (last 10 years): roughly 55-60% annualised (but with 70-80% drops along the way).

- Ethereum (last 10 years): roughly 70-85% annualised (with similar major drops).

- Top-20 altcoins (mixed performance): some went 50-100x, many went to near zero. Very hard to predict which.

- Random small altcoins: most have lost 90%+ of value from their peak.

Translation — ₹1 lakh invested in Bitcoin 10 years ago (in 2016, at around $450 per BTC) could be worth ₹1-2 crore today. But you would need to have held through 80% drops twice (2018 and 2022) without panic selling. Most people did not.

The honest interpretation.

Crypto has produced bigger absolute returns than stocks over this specific window. But:

1. You cannot predict crypto's future returns. Past 60% annualised returns do not guarantee future returns anywhere close to that. Stocks have 150+ years of consistency. Crypto has 17 years of wild swings.

2. Crypto's drawdowns are brutal. Any serious crypto investor has lived through at least one 70-80% drop. Many sold at the bottom and missed the recovery.

3. Survivorship bias is huge in crypto. We remember the Bitcoin success story. We forget the thousands of coins that went to zero. If you had randomly picked 10 crypto coins in 2016, statistically most would have been worthless by now.

4. Stock returns are more reliable. A diversified equity mutual fund has never failed to recover over any 10-year period in Indian history. It moves slower, but it is more predictable.

For most long-term wealth, stocks are the foundation. For the growth boost, a small crypto allocation makes sense — if you can tolerate the volatility. Our portfolio management guide covers exact allocation percentages for different risk profiles.

Volatility and risk — how much can you lose

Returns are only half the story. Risk is the other half. And crypto and stocks have very different risk profiles.

Time and volatility compared — crypto never sleeps, stocks have guardrails.

Stock market volatility — what to expect:

A typical Indian equity mutual fund has annual volatility around 15-20%. What does that mean? In a bad year, it might drop 20-30%. In a really bad year (like 2008 or March 2020), it might drop 35-40%. In a great year, it might rise 30-40%. Most years, it moves gently between -15% and +25%.

The Indian stock market has circuit breakers — if a major index falls more than 10% in a single day, trading is paused. This prevents panic cascades. Crypto markets have no such protection.

Historical major drops in Indian stocks:

- 2008 financial crisis: Sensex fell ~60% (peak to trough, over roughly 12 months). Recovered fully within 2 years.

- March 2020 COVID crash: fell ~38% in 3 weeks. Recovered within 8 months.

- 2015-16 China slowdown: fell ~22% over 8 months. Recovered within 12 months.

Even the worst cases — stocks recover. Patient investors who did not panic sell made it through every crisis.

Crypto volatility — what to expect:

Bitcoin's annual volatility is around 70-85%. That is 4-5 times higher than stocks. What does this mean practically?

In any given year, Bitcoin can:

- Drop 40-50% in a few weeks during a bear phase

- Rise 100-300% in a few months during a bull phase

- Drop 20% in a single day during crashes

- Rise 15-20% in a single day during rallies

Historical major drops in crypto:

- 2018 crypto winter: BTC fell 84% peak to trough. Altcoins fell 90-99%.

- 2022 crypto bear: BTC fell 77%. Many altcoins went to zero (LUNA collapsed from $119 to $0.0001 in days).

- March 2020: BTC fell 50% in 2 days.

- May 2021: BTC fell 55% in 3 weeks.

These are not minor corrections. These are devastating drops that destroy unprepared investors emotionally and financially.

The psychological dimension.

Numbers alone do not capture the experience. Watching your ₹1 lakh become ₹30,000 in 3 weeks, while Twitter is full of people calling it "just getting started", breaks most investors. Many sell at the bottom — right before the recovery.

Stock investors rarely go through this. A 30% drop feels bad but is recoverable. A 70% drop on a leveraged crypto position is often unrecoverable — emotionally and financially. Our market psychology guide explains why extreme volatility is the main reason most retail crypto traders lose money — not bad picks, but bad timing driven by emotion.

Smaller is better for crypto.

This is why financial advisors recommend keeping crypto to a small percentage of net worth (2-10% for most Indian investors). If you lose 70% of a 5% allocation, your total portfolio is down 3.5%. Recoverable. If you lose 70% of a 50% allocation, your total portfolio is down 35%. Much harder to recover from emotionally.

For stocks, you can comfortably hold 40-60% of your investable wealth. For crypto, comfortable means much less. That is just the math of volatility and survival.

Tax and liquidity — the hidden costs

Most beginners focus on returns. They forget taxes. Over decades, tax treatment can make bigger differences than gross returns. Here is how Indian tax rules compare.

Indian stock tax — favourable:

- Long-term capital gains (LTCG): holdings over 1 year pay 10% on gains above ₹1 lakh per year. Very investor-friendly.

- Short-term capital gains (STCG): holdings under 1 year pay 15% flat.

- Dividends: taxed at your slab rate (added to income). Usually 10-30% depending on income level.

- Losses: short-term losses can offset any gains. Long-term losses can offset long-term gains only. Losses can be carried forward up to 8 years.

- SIP-friendly: systematic investments benefit from indexation benefits on debt funds.

For most retail investors, long-term stock investing results in very low effective tax rates — often 5-10% of gains after accounting for the ₹1 lakh annual exemption.

Indian crypto tax — brutal:

- Flat 30% tax on all profits regardless of holding period. No long-term benefit.

- No slab benefit — same 30% whether you make ₹50,000 or ₹50 lakh.

- 4% cess on the tax amount (effective 31.2%).

- 1% TDS deducted automatically on every sale by Indian exchanges.

- No loss offset: crypto losses cannot be offset against stock gains, salary, or any other income. Cannot be carried forward either.

- Every swap is taxable: converting BTC to ETH triggers a tax event, even though no INR was received.

- No deductions: trading fees, internet bills, research costs — none are deductible.

Our crypto tax guide covers this in full detail with calculations. The crucial point: crypto's tax regime eats a significantly larger share of profits than stocks.

Real comparison — ₹1 lakh profit scenario:

- Stock held over 1 year, ₹1 lakh LTCG: no tax (within the ₹1 lakh exemption). You keep ₹1,00,000.

- Stock held over 1 year, ₹2 lakh LTCG: tax on the ₹1 lakh above exemption = ₹10,000. You keep ₹1,90,000 out of ₹2,00,000 profit.

- Crypto profit of ₹1 lakh: tax = ₹31,200 (including cess). You keep ₹68,800. Plus TDS was pre-deducted during the sale.

On the same ₹1 lakh gross profit, you keep ₹1,00,000 in stocks (if within exemption) vs ₹68,800 in crypto. That is a 31.2% tax drag on crypto vs 0% on stocks.

Liquidity — how fast can you access your money?

Stocks: Highly liquid during market hours (9:15 AM to 3:30 PM, Monday to Friday). Sell orders usually fill within seconds. Money appears in your bank account in 1-2 business days (T+1 settlement in India since 2023).

Crypto: Available 24/7 across global exchanges. You can sell at 2 AM on Sunday. However, Indian exchanges have variable INR withdrawal times — ranging from instant to 24 hours. Larger amounts may take longer due to regulatory checks.

For quick emergency access, stocks win slightly (instant during market hours, crypto has some withdrawal delays). For overnight or weekend access, crypto wins (stocks are closed).

Neither is "bad" for liquidity. Both are fine for most investors. But crypto's round-the-clock availability also means you can make panicked decisions at 3 AM — a double-edged blade.

Market hours and access — 24/7 vs 9:15-3:30

One of the biggest lifestyle differences between crypto and stock investing is when the markets are open.

Indian stock market — structured hours:

- Pre-open session: 9:00 AM to 9:15 AM (limited orders)

- Normal trading: 9:15 AM to 3:30 PM, Monday through Friday

- Closed: weekends, about 12-15 national holidays per year

- Circuit breakers: trading pauses if major indices fall more than 10% in a day

This structure has big implications. You cannot trade stocks after 3:30 PM. You cannot trade on weekends. Major news that breaks Saturday night cannot affect your portfolio until Monday's open — giving you time to think calmly about any reaction.

The closed hours also prevent panic reactions. In crypto, you can open your phone at 2 AM, see a crash headline, panic-sell at the worst possible moment. In stocks, the market is closed — you cannot act until morning, by which point you may have calmed down.

Crypto market — continuous:

- Open: 24 hours, 7 days, 365 days

- No holidays: Diwali, Christmas, your birthday — crypto trades

- No circuit breakers: prices can free-fall 30-40% in a few hours without pauses

- Global: major moves often happen during US market hours (evening in India) or Asian hours (morning in India)

This sounds like freedom. For some people, it is. You can trade anytime that fits your life. You do not need to take lunch breaks at the office to watch charts.

But the 24/7 nature also creates problems:

1. You can never mentally escape. Many crypto investors find themselves checking prices constantly — morning, lunch, evening, before bed, during sleep interruptions. This is mentally exhausting and often leads to overtrading.

2. Major moves happen while you sleep. You wake up Monday to find BTC dropped 15% overnight. Stock investors are protected from overnight moves (since there is no overnight trading). Crypto investors live with constant exposure.

3. Weekend moves are often extreme. With lower liquidity on weekends (less professional activity), crypto often moves more dramatically. Sunday night crashes are common.

4. No cooling-off period. In stocks, a breaking Friday afternoon story has the whole weekend for you to research calmly before acting Monday. In crypto, you can impulsively react in 30 seconds — usually to your detriment.

Lifestyle fit — which suits you?

- Busy professionals who want "set and forget" investing: stocks + mutual funds fit better. The closed market hours are a feature, not a bug. You are not tempted to check constantly.

- Night owls, shift workers, or anyone who cannot easily trade during 9:15-3:30: crypto's 24/7 access is genuinely useful. You can invest on your own schedule.

- Students or young people: crypto's lower entry barrier (no demat account needed initially, can start with ₹100) appeals. But the volatility danger is real.

- Retirees: stocks' structured hours and lower volatility suit better. Do not chase crypto's excitement at the cost of sleep.

For most beginners, I suggest using stocks as your main investing approach and crypto as a small side allocation (5-15%). This way, the bulk of your portfolio benefits from the structured, cooler-headed stock market, while crypto lets you participate in the upside without dominating your attention.

How to combine both in one portfolio

The final and most important question — how should an Indian investor actually combine both? Forget "which is better". Think about "how should I use both intelligently"?

A sample Indian investor's allocation — crypto as a small slice, not the whole plate.

The 60-25-15 framework for moderate investors (age 30-45).

This is a common, sensible allocation for most middle-class Indian professionals:

- 60% — Indian equity: Nifty 50 index funds, well-diversified mutual funds, blue-chip stocks like HDFC Bank, Reliance, TCS, ITC, Infosys. This is your wealth foundation.

- 25% — Fixed income and safety: fixed deposits, PPF, debt mutual funds, emergency fund. This provides stability.

- 15% — Crypto: split as 60% Bitcoin, 25% Ethereum, 15% top altcoins (and stablecoins as ready cash). This is your growth booster.

For a ₹10 lakh portfolio, that means: ₹6 lakh in stocks/mutual funds, ₹2.5 lakh in safety instruments, ₹1.5 lakh in crypto.

Conservative variation (age 45+ or low risk tolerance).

- 50% Indian equity (more diversified funds, less individual stock picking)

- 40% fixed income (FD, PPF, debt funds)

- 5-10% crypto (mostly BTC, minimal altcoins)

Aggressive variation (age 20-30 with long horizon).

- 60% Indian equity (can include mid-caps and small-caps for growth)

- 15% fixed income (emergency fund + some safety)

- 20-25% crypto (still diversified within crypto: 50% BTC/ETH, 25% stablecoins, 25% altcoins)

Notice — even the most aggressive plan keeps crypto at 25% maximum. This is not because crypto is bad. It is because when (not if) crypto crashes 70%, you need to survive to see the recovery. 25% of a portfolio becoming 7.5% hurts but is recoverable. 70% becoming 20% can financially ruin you.

How to actually build this over time.

Do not rush to reach your target allocation immediately. Build it over 6-12 months through regular investing. A sample monthly investment plan:

Say you can invest ₹20,000 per month. Split it:

- ₹12,000 (60%) → Nifty 50 index fund SIP and/or 2-3 quality equity mutual funds

- ₹5,000 (25%) → PPF, FD, or debt mutual fund SIP

- ₹3,000 (15%) → Bitcoin and Ethereum (₹2,000 BTC + ₹1,000 ETH, weekly or monthly)

This approach is basically dollar-cost averaging across both asset classes. You buy during highs and lows. Over years, you build a balanced portfolio without trying to time markets.

Rebalancing between stocks and crypto.

Every 6-12 months, check your actual percentages. If crypto has boomed and now represents 35% of your portfolio (target was 15%), sell some crypto and buy more stocks to rebalance. If crypto has crashed and now represents 5%, you may consider buying more crypto to rebalance up to 15%.

Rebalancing forces you to sell high (take profits from whatever went up) and buy low (buy more of whatever went down). This is mathematically how you beat most traders over long periods — without prediction, just discipline.

KAVACH — Balance crypto with the rest of your wealth

KAVACH is our capital protection framework covering asset allocation, risk-adjusted position sizing, tax-aware portfolio construction, and the discipline of rebalancing across asset classes. If you are building real wealth (not gambling), the structure matters more than any single pick.

Explore the Store →A final honest thought. I have seen countless Indian investors ruin themselves by treating crypto and stocks as an either/or choice. The successful investors I know treat them as complementary. Stocks are the slow, steady engine of wealth. Crypto is a small, high-growth addition. Together, they balance each other. Alone, each has weaknesses. Together, the portfolio benefits from both worlds without being destroyed by either.

Read our crypto vs mutual funds comparison for another angle on the trade-offs. Our portfolio management guide has detailed allocation templates for different life stages. Start balanced. Stay balanced. Adjust as you learn. That is how most successful Indian wealth builders actually do it.

Join our Telegram community where we discuss portfolio ideas and rebalancing approaches. Our crypto education courses include modules on combining asset classes for Indian investors. Do not pick sides. Use both.

Frequently Asked Questions

Is crypto riskier than the Indian stock market?

Yes, significantly. Crypto volatility is 4-5 times higher than stock volatility. Bitcoin has fallen 70-85% multiple times; Indian equity indexes have rarely fallen more than 40% even in the worst crises. Altcoins can go to zero completely, while diversified stock portfolios have never failed to recover over any 10-year period in Indian history. Most financial advisors recommend limiting crypto exposure to 5-15% of your total investments.

Are crypto returns really higher than stock market returns in India?

Over the past 10 years, yes — Bitcoin has outperformed Indian stocks by a significant margin. However, past returns do not guarantee future results. Bitcoin's 55-60% annualised returns came with 70-80% drawdowns that most investors could not emotionally survive. Indian equity's 12-13% annualised returns came with far smaller drawdowns. Crypto's higher returns exist precisely because of higher risk — not despite it.

Can I invest in both crypto and stocks from India legally?

Yes. Indian investors can legally invest in both domestic stocks (through SEBI-regulated brokers and demat accounts) and crypto (through Indian exchanges or P2P with tax compliance). Both require PAN and KYC. Both are subject to taxation — stocks at favourable 10-15% rates on capital gains, crypto at 30% flat plus 1% TDS on sales. Indian law currently permits both but treats them very differently.

What percentage of my portfolio should be in crypto vs stocks?

For most Indian investors, a sensible allocation is 60% equity, 25% fixed income, and 5-15% crypto. Conservative investors or retirees should keep crypto to 0-5%. Aggressive young investors can go up to 20-25%. Never put more than you can afford to lose 70% of in crypto — that is a realistic bear-market drawdown. Our crypto portfolio management guide covers allocation frameworks in more detail.

How does crypto tax compare to stock tax in India?

Crypto tax is significantly harsher. Stocks pay 10% LTCG on gains above ₹1 lakh per year (after 1-year holding), or 15% STCG if sold sooner. Crypto pays flat 30% plus 4% cess (effective 31.2%) on all profits regardless of holding period. Plus 1% TDS is deducted on every crypto sale. Crypto losses cannot be offset against stock gains, salary, or any other income — unlike stock losses which offer full offset flexibility.

This article is for educational purposes only and does not constitute financial advice. Crypto investments are subject to market risk and are not regulated by SEBI or RBI in India. Past performance does not guarantee future results. Always do your own research, consult a registered financial advisor, and never invest more than you can afford to lose. cRyPtO sMaRt and Avik Kanrar are not liable for any trading decisions or losses based on this content.