What is DeFi in simple words?

DeFi is short for Decentralized Finance. It is a new way to do financial things — like saving, borrowing, and trading — without using a bank or broker.

Let me explain with an example. When you put ₹10,000 in a savings account at your bank, the bank holds your money. The bank decides how much interest you get. The bank decides if you can withdraw. The bank decides when it is open or closed. You trust the bank with your money.

In DeFi, you do the same thing — but there is no bank. Instead, computer code holds your money. The code decides the rules (which are public and cannot be changed secretly). The code runs 24 hours a day, 7 days a week. You trust the code, not a company.

This computer code is called a smart contract. A smart contract is just a program that runs on a blockchain (a special type of computer network, the same kind Bitcoin runs on). When you interact with a smart contract, you are interacting with a program — not a person.

Here is what makes DeFi special:

- Open to everyone. You do not need permission from anyone. You just need an internet connection and a crypto wallet.

- Open 24/7. Banks close on Sundays and holidays. DeFi never closes.

- Transparent. All transactions are public. You can see everything that is happening.

- No middleman. The code directly connects lenders and borrowers, buyers and sellers.

But DeFi is not magic. It has real risks (we will cover them later). And it is not a replacement for all banking — yet. Right now, DeFi is useful for specific things like lending, trading, and earning interest on crypto. Think of it as a set of new financial tools, not a complete replacement for your bank.

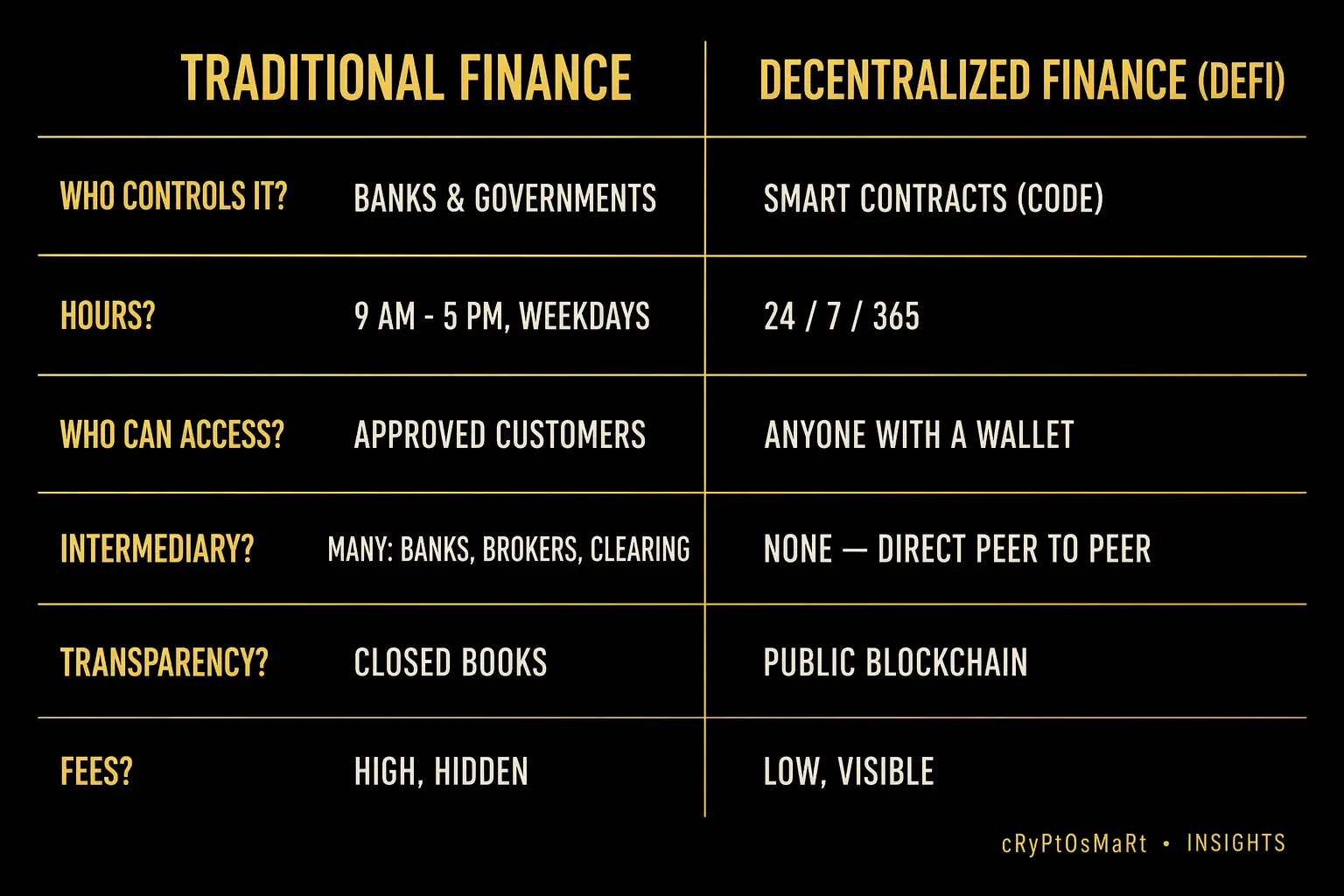

How DeFi is different from regular banks

Before we go deeper, let us compare DeFi with the banks you already know. Regular banking is sometimes called TradFi (short for traditional finance). Here is how they stack up.

Traditional finance vs DeFi — six key differences that change how money works.

Who controls it?

TradFi: Banks and governments. They make the rules. They can freeze your account. They can block transfers.

DeFi: Smart contracts (code). The rules are public and cannot be changed without most users agreeing. No single company or government can freeze your money.

When is it open?

TradFi: Weekdays, business hours. Closed on Sundays and holidays. International transfers take 2-5 business days.

DeFi: 24 hours a day, 7 days a week, 365 days a year. Transfers happen in seconds or minutes, not days.

Who can use it?

TradFi: Only approved customers. You need ID proof, address proof, income proof, sometimes credit checks. Many people globally are excluded.

DeFi: Anyone with internet and a wallet. No permission needed. A farmer in Odisha and a banker in Singapore have equal access.

Are there middlemen?

TradFi: Many. Banks, brokers, clearing houses, payment processors. Each takes a small fee.

DeFi: Almost none. You transact directly with a smart contract. There is a small network fee (called "gas"), but no middleman profits.

Is it transparent?

TradFi: No. Your bank keeps its records private. You only see your own account.

DeFi: Yes. Every transaction is recorded on the public blockchain. Anyone can verify anything.

What about fees?

TradFi: Often hidden. Account maintenance, failed transaction, foreign exchange spread, minimum balance penalties.

DeFi: Visible. Every fee is shown upfront before you confirm a transaction.

This does not mean DeFi is automatically better. Banks offer things DeFi cannot — physical branches, customer support in your local language, legal protection if something goes wrong. DeFi offers different things — freedom, speed, and global access. Both have a role to play.

Smart contracts — the engine of DeFi

Everything in DeFi runs on smart contracts. So let us understand them properly.

A smart contract is a program that runs on a blockchain. It has rules written into its code. When certain conditions are met, the program automatically takes action. No human is needed to execute it.

Imagine a vending machine. You put ₹50 in. You press a button for a cold drink. The machine checks: "Has the user paid ₹50? Yes. Is the drink available? Yes." Then it releases the drink. No shopkeeper needed. The machine does it automatically, based on pre-set rules.

A smart contract is the same idea, but for money and finance. Example rules a smart contract might have:

- "If user deposits 1 ETH, give them 2,500 USDC back as a loan, and lock the 1 ETH as collateral."

- "Every hour, take 0.01% interest from the borrower and give it to the lender."

- "If the ETH price drops below $2,000, sell the collateral automatically to repay the loan."

Once the smart contract is deployed, it runs these rules forever — automatically, publicly, and without anyone needing to push a button. The code is the rule. The code is also the executor of the rule.

Why this is powerful. Because the rules are public, you can read them before using the contract. You know exactly what will happen to your money. Unlike a bank, which can change its rules in the fine print next year, a smart contract cannot quietly change its behaviour.

Why this is risky. Because the code is the final authority, a bug in the code is also final. If a smart contract has a flaw, hackers can exploit it and steal user funds. Once the money is stolen, there is no customer service to call. No government agency to file a complaint with. This is why security audits and proven track records matter so much in DeFi. Always use smart contracts that have been audited and have been running safely for at least a year or two.

The six building blocks of DeFi

DeFi is not just one thing. It is a whole ecosystem of different tools. Here are the six main building blocks.

The DeFi ecosystem — six building blocks that together recreate traditional finance on blockchain.

1. Decentralized Exchanges (DEXs). A DEX is a place to swap one crypto for another without an exchange company holding your money. Popular examples: Uniswap, PancakeSwap. You connect your wallet, pick the coin you have and the coin you want, and the DEX swaps them directly. You never deposit with them.

2. Lending and Borrowing. Platforms like Aave or Compound let you lend your crypto to earn interest, or borrow against your crypto. The interest rates change based on supply and demand — the more people lending, the lower the rate, and vice versa.

3. Staking. Staking means locking your coins to help secure a blockchain network, and getting rewards in return. It is similar to earning interest in a fixed deposit, except you are supporting a network instead of a bank. Typical returns: 3-8% per year.

4. Stablecoins. Stablecoins are crypto coins whose price stays equal to one US dollar (or ₹, in some versions). Examples: USDT, USDC, DAI. They are crypto's version of "cash". Most DeFi activity happens using stablecoins, not Bitcoin or Ethereum directly. We will cover these in more detail in the next section.

5. Yield Farming. This is the more advanced cousin of lending. You provide liquidity (both sides of a trading pair) to a DEX and earn fees from every trade that happens on that pair. The returns can be high (10-50% per year), but so can the risks. Yield farming is not for absolute beginners.

6. Derivatives. Futures, options, and other complex financial products — but running on smart contracts instead of traditional exchanges. These are very advanced and risky. Avoid them until you are comfortable with all the other building blocks.

As a beginner, start with just two building blocks: DEXs (for swapping coins) and lending/staking (for earning interest). These two cover 80% of what a new DeFi user needs. The other four can wait until you are experienced.

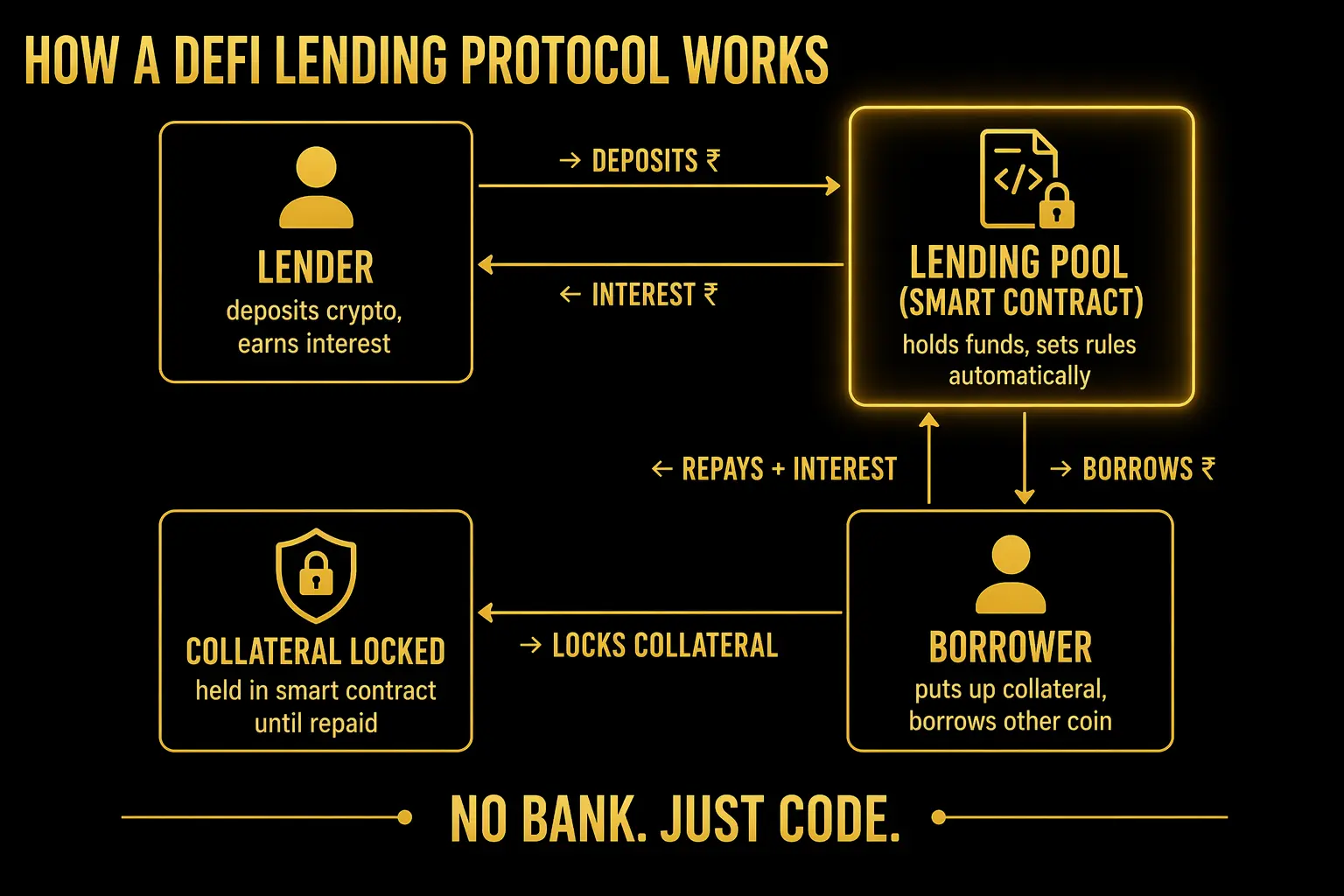

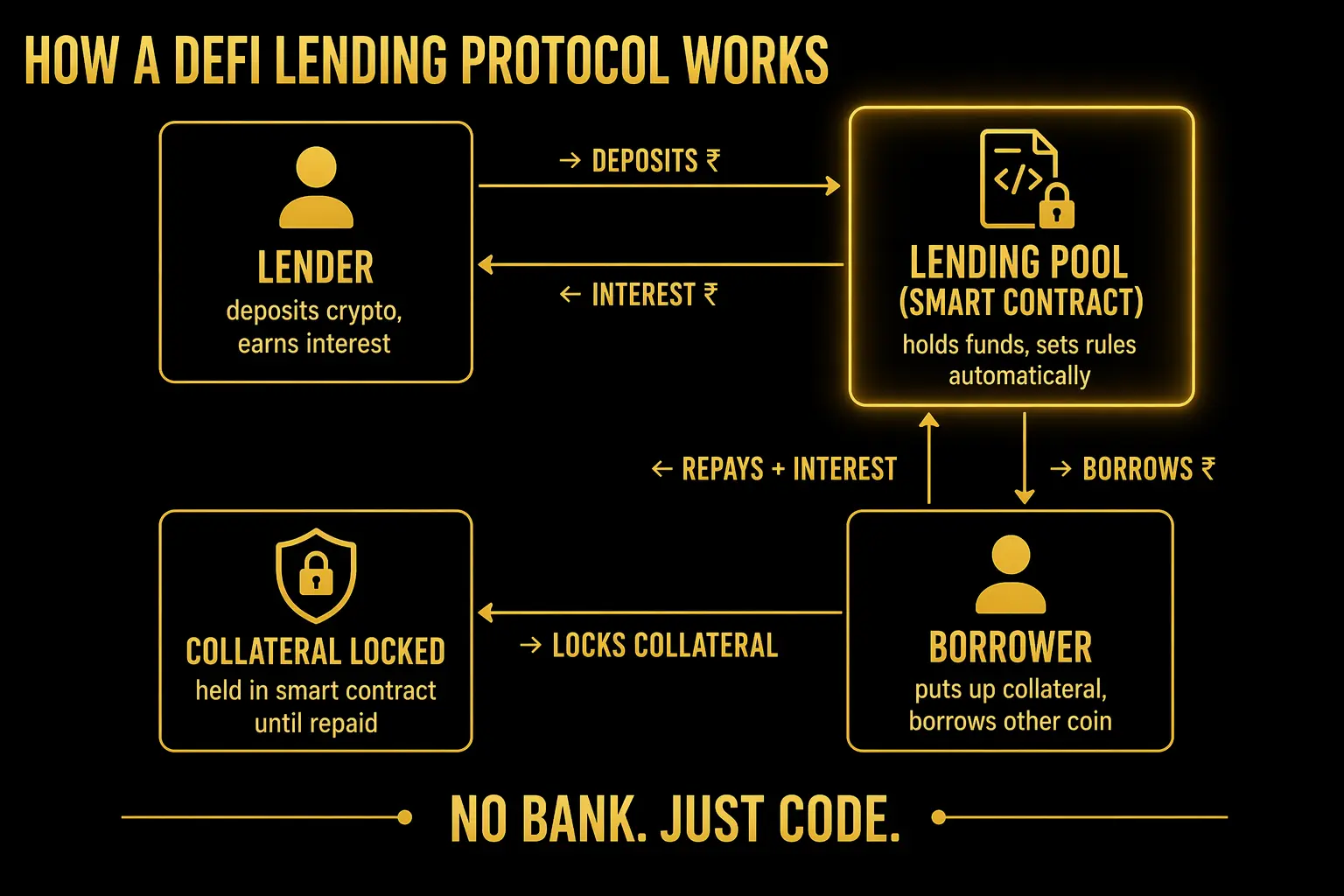

How DeFi lending actually works

Let us walk through the most common DeFi activity: lending. Say you have some USDC (a stablecoin worth $1 each). You want to earn interest on it. Here is what happens when you lend it out.

The four-way flow of a DeFi loan — lender, pool, borrower, and locked collateral.

Step 1. You connect your crypto wallet to a lending platform like Aave. You deposit 1,000 USDC into the lending smart contract.

Step 2. Your USDC joins a big pool with thousands of other lenders' USDC. The pool is now, say, 50 million USDC available for borrowing.

Step 3. Somewhere in the world, another person wants to borrow USDC. They do not want to sell their Bitcoin because they believe it will go up. Instead, they put 1 BTC (worth, say, $60,000) into the smart contract as collateral. Collateral means a guarantee — if they fail to repay, the contract takes their BTC.

Step 4. The contract calculates how much they can borrow. For safety, the contract only lets them borrow up to 70% of their collateral value. So on $60,000 of BTC, they can borrow up to $42,000 USDC. Say they borrow $30,000.

Step 5. The borrower gets their $30,000 USDC. They pay interest to the pool — say 8% per year, charged by the second.

Step 6. The interest flows back to all the lenders in proportion to how much they contributed. You, with your 1,000 USDC, earn your share — maybe 4-5% per year (less than what the borrower pays, because of fees and risk buffers).

Step 7. You can withdraw your money plus earned interest at any time. The smart contract lets you pull out as long as the pool has enough unborrowed funds — which it almost always does because only a small % of the pool is borrowed at any time.

What if the borrower's BTC falls in value? If BTC drops and the value of the collateral becomes too close to the borrowed amount, the smart contract automatically sells some of the BTC to repay the loan. This is called liquidation. You, the lender, are protected. You still get your money back, because the collateral was bigger than the loan.

This whole system runs without a single human intervening. It is the smart contract making loans, collecting interest, paying lenders, and liquidating bad loans — all automatically, 24/7.

Stablecoins — the money of DeFi

Most DeFi activity happens in stablecoins, not in Bitcoin or Ethereum. Understanding stablecoins is essential before you do anything in DeFi.

A stablecoin is a crypto coin whose price is designed to stay equal to a real-world currency — usually the US dollar. So 1 USDT = 1 USD. 1 USDC = 1 USD. Whether Bitcoin is at $50,000 or $70,000 today, 1 USDC still equals 1 USD.

Why do stablecoins exist? Because Bitcoin and Ethereum prices change every day. If you want to save or lend crypto without worrying about price swings, you need something stable. Stablecoins solve that.

Types of stablecoins you should know:

USDT (Tether). The oldest and most-used stablecoin. It is backed by a mix of cash and other assets held by the Tether company. Widely accepted but occasionally controversial.

USDC (USD Coin). Issued by Circle, a US regulated company. Backed 1:1 by cash and short-term government bonds. Generally considered the safest and most trusted stablecoin.

DAI. Different from the above. DAI is not backed by a company — it is backed by crypto collateral through smart contracts. It is more "decentralized" but its price can drift a little in rare situations.

Algorithmic stablecoins. These are NOT backed by real money. They use clever algorithms to try to stay at $1. Most of them have failed spectacularly. The famous Terra USD (UST) lost its peg in 2022 and went from $1 to near zero, wiping out billions. Avoid algorithmic stablecoins until you deeply understand the risks.

A simple rule for beginners: Stick with USDC for DeFi activities. It is audited regularly. It is transparent about its reserves. It has never lost its peg seriously. USDT is a fine second choice. Everything else is optional.

Indian users should note: stablecoins follow the same 30% tax rule as any other crypto in India, plus 1% TDS on every sell. Our crypto tax guide covers the details. Also, understanding what makes any coin valuable matters a lot — our tokenomics guide is a good next read.

The real risks of DeFi (be honest)

Nobody will help you understand the risks better than we will. DeFi has real rewards, but it also has real dangers. Here are the ones you must know.

Risk 1 — Smart contract bugs. If a smart contract has a flaw, hackers can exploit it and drain user funds. Billions of dollars have been lost this way since 2020. Reduce this risk by only using contracts that have been running safely for 2+ years and have multiple security audits.

Risk 2 — Rug pulls. Some DeFi projects are outright scams. Developers launch a token, attract deposits, then disappear with the money. New "hot" DeFi projects with no track record are the biggest trap. Our crypto scam guide explains how to spot these before you lose money.

Risk 3 — You are your own bank. If you lose your wallet password (called a "seed phrase"), your crypto is gone forever. No customer service can recover it. No government can get it back. This is the hardest part of DeFi for new users — the responsibility is entirely yours.

Risk 4 — Price volatility. Even in stablecoin-only DeFi activities, the underlying blockchain (like Ethereum) has volatility. If ETH drops a lot, borrower collateral can get liquidated in chain reactions that affect the whole ecosystem.

Risk 5 — Regulation uncertainty. India's regulatory stance on DeFi is still developing. While using DeFi is not illegal, taxation and reporting requirements can change. Always stay aware of current rules.

Risk 6 — Complex user experience. DeFi interfaces are not beginner-friendly. One wrong click, one wrong address, one typo — and your money can be gone. Always test with small amounts first before using big amounts.

Risk 7 — Gas fees on Ethereum. On the main Ethereum network, transaction fees (called "gas") can be very high — sometimes $20-$50 per transaction. For small amounts, this eats all your potential profit. Use cheaper networks like Polygon or Arbitrum for small DeFi activities.

None of these risks should stop you from exploring DeFi. But all of them should make you start small, learn carefully, and never put money you cannot afford to lose.

How to start with DeFi safely

If you want to try DeFi, here is the step-by-step path that minimises risk for beginners.

Step 1 — Get a crypto wallet. Download a free wallet like MetaMask (for Ethereum) or Phantom (for Solana). Write down your seed phrase on paper. Never share it with anyone. Never store it in WhatsApp, email, or cloud drive. If you lose this, you lose everything.

Step 2 — Buy a small amount of ETH or SOL. Start with just ₹1,000 to ₹5,000. You need some base crypto to pay for transaction fees. Buy from a known Indian exchange. Our Indian crypto buying guide shows how.

Step 3 — Transfer a small amount to your wallet. Send, say, ₹1,000 of ETH from the exchange to your wallet. Test with a very small amount first to make sure the address is correct.

Step 4 — Try one simple DeFi activity. The safest first activity is lending USDC on a well-known platform. Swap a little ETH for USDC, then deposit it into Aave on Polygon network (low fees). Watch how the interest builds up over days. Get familiar with the flow.

Step 5 — Practice for 2-3 months before scaling up. Start small. Make mistakes with small amounts. Learn by doing. Only increase your DeFi exposure after you feel completely comfortable with the basic flow.

Step 6 — Keep learning. DeFi changes fast. New protocols appear, old ones die, best practices evolve. Stay connected to communities and educational resources to avoid using outdated information.

VIDYA MANDAL — Learn DeFi properly before you risk real money

VIDYA MANDAL is our structured knowledge library covering DeFi step-by-step — wallet setup, stablecoins, lending, staking, and how to avoid the common traps that drain beginner wallets. If you want to explore DeFi, learning the fundamentals first will save you a lot of expensive mistakes.

Explore the Store →Final thought. DeFi is genuinely revolutionary. It is the first real experiment in open, permissionless finance. For Indian users especially — where access to international finance products is often restricted — DeFi offers genuine new possibilities. But it rewards the patient and punishes the reckless. Go slow. Learn deeply. Use small amounts. The opportunity will still be here in a year, when you are ready.

Join our Telegram community where beginners share their DeFi questions in a judgment-free space. Our crypto education courses include a DeFi module that walks through real hands-on steps with small practice amounts.

Frequently asked questions

Is DeFi legal in India?

Using DeFi is not illegal in India, but the regulatory environment is still evolving. Any profit you make from DeFi activities is taxed at the same 30% flat rate as other crypto, with 1% TDS applied on transactions where applicable. Always track your DeFi activity carefully for tax filing. Rules can change, so stay informed about current regulations.

How much money do I need to start with DeFi?

You can start with as little as ₹2,000-₹5,000 for learning purposes. However, on Ethereum main network, transaction fees can be high ($10-30 each), so small amounts are not cost-effective there. Use cheaper networks like Polygon or Arbitrum for small beginner experiments. Once comfortable, realistic DeFi participation starts around ₹20,000-50,000.

Can I lose all my money in DeFi?

Yes, in specific ways: smart contract hacks, rug-pull scams, losing your wallet seed phrase, or using unverified protocols. Stick to well-known protocols that have been running safely for 2+ years, use stablecoins for your first experiments, and never risk money you cannot afford to lose. Start with ₹2,000 experiments before scaling up.

What is the difference between DeFi and a crypto exchange?

A crypto exchange like CoinDCX or WazirX holds your money and executes trades for you. If the exchange gets hacked or fails, your money may be lost. In DeFi, you hold your own money in your wallet and interact directly with smart contracts. There is no company holding your funds — but this also means you are fully responsible for your wallet security.

Which is safer — Bitcoin or DeFi?

Bitcoin is simpler and has fewer layers where things can go wrong, so it is safer from a technical standpoint. DeFi involves smart contracts that can have bugs, protocols that can fail, and a complex user interface where mistakes cost money. Beginners should spend time with Bitcoin and understand crypto basics thoroughly before exploring DeFi.

cRyPtO sMaRt is not registered with SEBI and does not provide investment advice. Crypto trading carries significant risk of capital loss. The strategies, examples, and opinions shared in this article are for educational purposes only. Always do your own research and consult a SEBI-registered financial advisor before investing real capital. Past performance does not guarantee future results.