- Why choosing the right exchange matters

- Types of crypto exchanges explained

- The Indian crypto exchange landscape

- Security — what to check before you trust them

- KYC and regulatory compliance

- Fees — what you actually pay

- Features that matter for beginners

- Red flags that should make you run

- Frequently asked questions

Why choosing the right exchange matters

A crypto exchange is a website or app where you buy and sell cryptocurrency using INR. Think of it like the stock broker of crypto. Just like you need an account with Zerodha or Upstox to trade stocks, you need an exchange to trade crypto.

Here is why this choice matters more than most beginners realise. Your exchange is where your money lives. Where your KYC documents go. Where every trade is tracked and taxed. A bad exchange choice can cost you money through high fees, poor security, slow withdrawals, or — in the worst case — complete loss of funds if the exchange collapses.

Remember, in November 2022, FTX was one of the world's largest crypto exchanges. It collapsed overnight. Millions of users lost everything. Closer to home, WazirX faced major challenges in 2024 after a hack involving hundreds of crores worth of user funds. These stories are not rare warnings — they are regular patterns in crypto.

The good news is that choosing a safe, reliable exchange is not complicated. You just need to know what to check. Most beginners pick an exchange based on advertisements or friend recommendations — then regret it when they discover hidden fees, withdrawal delays, or security gaps.

This guide walks through every factor you need to evaluate. You will learn:

- What security features actually matter (and which are just marketing)

- How Indian KYC and TDS compliance work

- How to compare fees honestly (spreads matter more than headline rates)

- Which features are essential for beginners vs optional

- How to spot red flags before losing money

By the end, you will be able to confidently pick an exchange that fits your situation — not just the one with the biggest billboard ad. And you will know when to split funds across multiple exchanges for better safety.

One important note — this guide does not recommend any specific exchange. Exchange quality changes over time. Customer support that is excellent in 2026 may be terrible by 2027. Security practices change. Regulations change. What stays constant are the questions you should ask. This guide teaches the questions, not the answers. Apply the questions to any exchange you are considering, whenever you are considering it.

Types of crypto exchanges explained

Not all crypto exchanges are the same. There are three main types, each with different trade-offs. Understanding these helps you pick the right fit.

1. Centralised exchanges (CEX) — easiest for beginners.

A centralised exchange is a company that runs a platform where people buy and sell crypto. The company controls everything — the order book, your account, your KYC, your crypto balance. Examples from India include CoinDCX, WazirX, ZebPay, Mudrex, and Bitbns.

Pros:

- Easy to use — simple apps and websites

- Direct INR deposits through UPI, bank transfer, IMPS

- Customer support available for issues

- Automatic tax and TDS handling for Indian users

- Large selection of coins

Cons:

- Your crypto lives on their servers (they control your keys)

- If the exchange is hacked or collapses, you can lose everything

- Subject to account freezes, withdrawal limits, and KYC delays

- Requires full personal identity disclosure

For 99% of Indian beginners, centralised exchanges are the right starting point. They handle the complex parts of crypto (INR deposits, tax reporting, coin custody) so you can focus on learning.

2. Decentralised exchanges (DEX) — advanced option.

A decentralised exchange is not a company — it is a set of smart contracts on a blockchain (like Ethereum or BSC). You trade directly from your own wallet. There is no account, no KYC, no customer support.

Examples: Uniswap, PancakeSwap, 1inch, SushiSwap.

Pros:

- You control your own keys — no exchange can freeze or lose your funds

- Access to thousands of coins not listed on centralised exchanges

- No KYC requirements

- Global access

Cons:

- Cannot deposit INR directly — you must already have crypto to use them

- More complex interface, higher chance of making costly mistakes

- No customer support

- Gas fees can be expensive

- Higher chance of being scammed by fake tokens or malicious contracts

- Tax reporting is your own responsibility

DEXes are not recommended for beginners. Start with a centralised exchange. Move to DEXes only after 1-2 years of experience.

3. Peer-to-peer (P2P) platforms — specific use cases.

P2P platforms match buyers and sellers directly, with the platform acting as escrow during the trade. You can buy crypto using UPI, bank transfer, or cash from another person rather than a company.

Examples: Binance P2P, Koinbazar, LocalBitcoins (now defunct).

Pros:

- Can work when bank channels to exchanges are disrupted

- Sometimes better rates than centralised exchanges

- Multiple payment options

Cons:

- Higher risk of scams from fake buyers or sellers

- Variable pricing — spreads can be wide

- Tax reporting can be complicated

- Bank accounts receiving crypto-related funds have been frozen in India in some cases

P2P is useful for specific situations but adds risk. Not recommended as your primary way to buy crypto unless you have specific reasons.

For the rest of this guide, we will focus on evaluating centralised exchanges — the main choice for Indian beginners. The same security principles apply to other types too.

The Indian crypto exchange landscape

Before comparing specific exchanges, let me describe the Indian exchange landscape in 2026. It will help you understand what to expect.

The major Indian-headquartered exchanges.

Several Indian exchanges have emerged over the past few years. They are all domestically operated, comply with Indian tax laws (30% tax + 1% TDS handled automatically), and offer direct INR deposits. Their features, fees, and coin selections vary considerably. They compete mainly on ease of use, coin variety, fees, and customer support quality.

What they generally offer:

- Direct INR deposits via UPI, IMPS, bank transfer

- Trading in 100-500+ cryptocurrencies

- Mobile apps for iOS and Android

- Automatic TDS deduction on sales

- Form 26AS reporting for tax filing

- Basic KYC required before trading

International exchanges accessible from India.

Large global exchanges like Binance, Coinbase, Kraken, and KuCoin technically accept Indian users. Some offer INR pairs through P2P, others require you to deposit crypto (not INR) to trade.

Pros of international exchanges:

- Generally lower fees

- Much wider coin selection

- Advanced features (futures, options, staking)

- Typically better liquidity

Cons for Indian users:

- No direct INR deposits (usually need P2P for funding)

- You are responsible for tax reporting and TDS compliance yourself (exchange will not deduct TDS automatically as Indian law requires)

- Customer support may be slow or unfamiliar with Indian concerns

- Regulatory uncertainty — if India tightens rules, access could change

- Bank transfers to fund international exchanges are sometimes flagged

For beginners, Indian exchanges are strongly preferred despite sometimes higher fees. The automatic compliance alone is worth it. Tax mistakes with crypto can cost you 10-50x what you save on fees.

What changed in India after 2022.

In the 2022 budget, India introduced specific crypto tax rules — 30% tax on profits, 1% TDS on sales, and strict reporting requirements. This had big effects on the exchange landscape:

- Daily trading volumes on Indian exchanges fell by 80-90% as many traders reduced activity.

- Some Indian exchanges closed or scaled back operations.

- Surviving exchanges invested heavily in compliance systems to handle TDS automatically.

- Many traders moved to international exchanges or P2P, increasing risk exposure.

- The exchanges that remained became more cautious about listing speculative coins.

The landscape is still evolving. The Financial Intelligence Unit (FIU-IND) has started requiring offshore crypto companies to register if they serve Indian users. Some have registered; others have been blocked. Always check current status before choosing any exchange. Our crypto tax guide covers the current regulatory environment in detail.

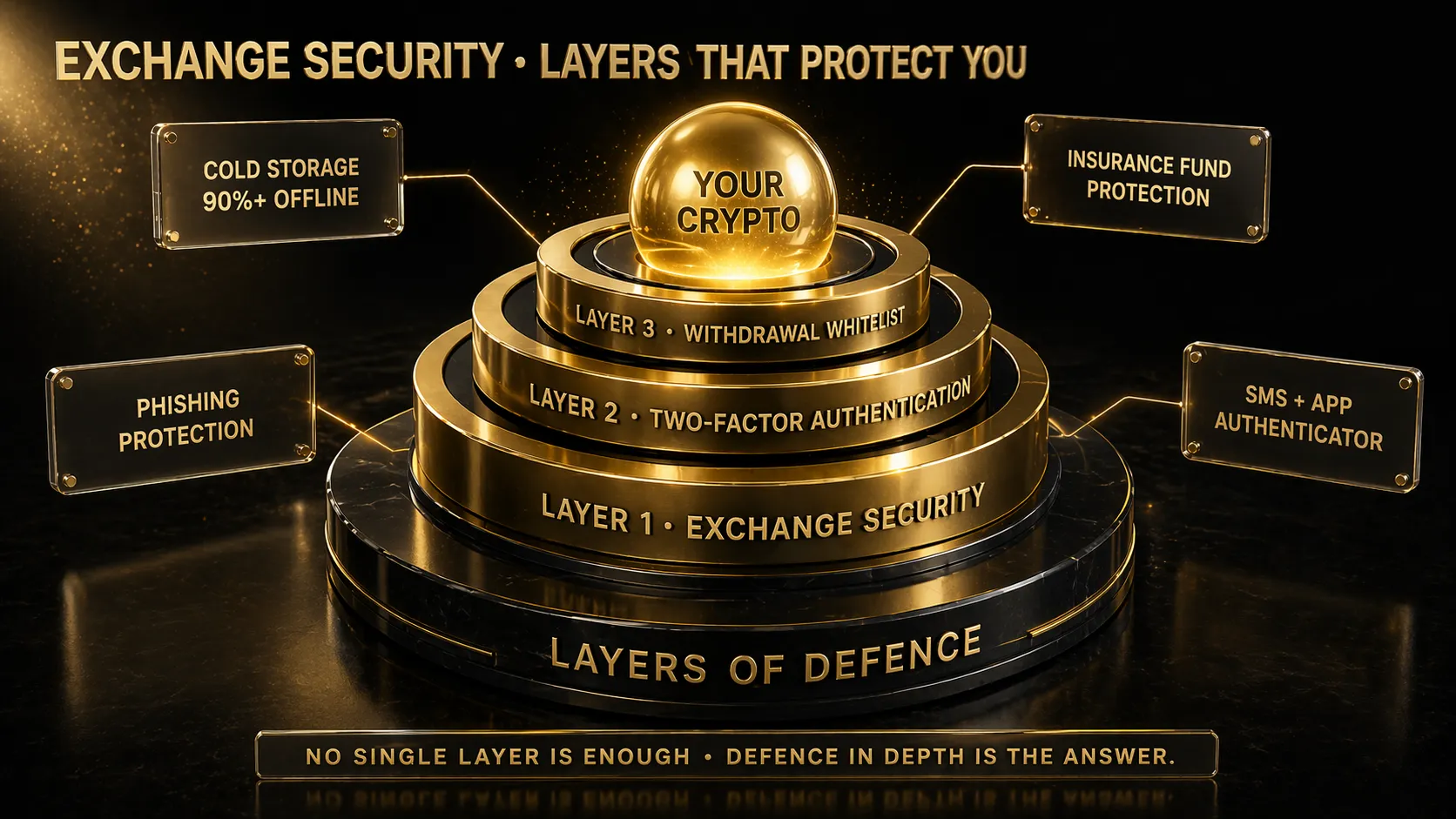

Security — what to check before you trust them

Security is the most important factor. Everything else — fees, features, coin selection — means nothing if you lose your money to a hack or collapse. Here is what to check.

Real exchange security is layered — no single mechanism is enough. Defence in depth is the only answer.

1. Cold storage percentage.

Good exchanges keep most user funds in "cold storage" — offline wallets not connected to the internet. Only a small percentage (typically 5-10%) is kept in "hot wallets" for daily operations. Cold-stored funds are nearly impossible to hack remotely.

What to look for:

- Exchange should publicly disclose what percentage of funds are in cold storage

- Look for claims like "95%+ in cold storage" or "multi-sig cold wallets"

- If the exchange does not disclose this at all, consider it a red flag

2. Insurance fund.

Some exchanges maintain a reserve fund to cover losses from security breaches. This is called an insurance fund or SAFU (Secure Asset Fund for Users). Binance popularised this concept; several Indian exchanges have similar reserves.

What to check:

- Is the insurance fund publicly disclosed with verifiable addresses?

- How large is the fund relative to total user deposits?

- Under what conditions will it be used?

An insurance fund does not guarantee full coverage in all scenarios, but it provides some protection beyond the exchange's basic reserves.

3. Proof of reserves.

After FTX's collapse in 2022, many exchanges started publishing "proof of reserves" — cryptographic proof that they actually hold the crypto they claim to hold on behalf of users. This is crucial for trust.

What to look for:

- Regular (monthly or quarterly) proof of reserves published

- Third-party audits by reputable firms

- Transparent wallet addresses that you can verify on-chain

An exchange that does not publish proof of reserves may be operating on fractional reserves — meaning they do not actually have enough crypto to cover all user balances. If a bank run occurs, funds cannot be returned. This is exactly what happened with FTX.

4. Two-factor authentication (2FA) options.

Good exchanges offer multiple 2FA options:

- Google Authenticator or Authy app (most secure)

- SMS (convenient but less secure — SIM swap attacks)

- Hardware keys like YubiKey (very secure, for advanced users)

Avoid exchanges that only offer SMS-based 2FA. SIM swap attacks (where criminals transfer your phone number to their SIM card) are common and can bypass SMS 2FA completely.

5. Withdrawal whitelist.

Major exchanges let you create a "whitelist" of addresses you can withdraw crypto to. Once enabled, withdrawals can only go to pre-approved addresses. Even if a hacker steals your login, they cannot withdraw your crypto to their own wallet.

If an exchange does not offer withdrawal whitelisting, that is a meaningful security gap.

6. Track record.

Check the exchange's past. Any major hacks? Any regulatory issues? Any customer fund losses? Google "[exchange name] hack" and "[exchange name] scandal" before opening an account.

Some history is acceptable if the exchange handled it well (full compensation to users, improved security). Some history is disqualifying (users lost funds, poor communication, ongoing legal problems).

7. KYC security.

You will be uploading PAN, Aadhaar, and bank details to the exchange. Their KYC document handling is critical. Check:

- Does their website use HTTPS (secure connection)?

- Do they have ISO 27001 certification or similar?

- Any history of KYC data leaks?

- How long do they retain documents?

KYC data leaks have happened with several Indian fintech companies. Your documents could end up on dark web forums if the exchange is careless. Our scam guide covers how leaked KYC data is often used for identity fraud and social engineering attacks.

KYC and regulatory compliance

For Indian users, regulatory compliance is not optional — it is required by law. An exchange that takes compliance seriously protects both itself and you.

What compliance looks like for Indian exchanges:

1. Full KYC process. Before trading, you must complete Know Your Customer verification. This typically requires:

- PAN card (mandatory)

- Aadhaar card or other government ID

- Bank account linked to the same PAN

- Live selfie or video verification

- Address proof (utility bill, rental agreement, or similar)

Full KYC usually takes 2-24 hours to approve. If an exchange lets you trade without KYC, it is either illegal or operating in regulatory gray zones. Avoid.

2. PMLA (Prevention of Money Laundering Act) compliance. Indian exchanges must report suspicious transactions and maintain records for regulators. This is a good thing — it means the exchange operates transparently within the legal system.

3. FIU-IND registration. The Financial Intelligence Unit requires crypto service providers serving Indian users to register. Registered exchanges are compliant with Indian reporting standards. Check the FIU-IND website for current registered entities.

4. TDS (Tax Deducted at Source) handling. Under Section 194S, a 1% TDS must be deducted on every crypto sale. Good Indian exchanges handle this automatically:

- TDS is calculated and deducted during the trade

- Deducted amount is deposited with the government under your PAN

- You receive Form 26AS showing total TDS paid annually

- You can claim TDS credit when filing your ITR

International exchanges do not do this automatically. If you use them, you are technically required to deduct and deposit TDS yourself — which is nearly impossible in practice. This is a major reason to prefer Indian exchanges.

5. Tax reporting support. Good exchanges provide:

- Downloadable transaction history (CSV or Excel)

- Annual profit/loss statements

- FIFO-based cost basis calculations

- Export formats compatible with ITR filing

Try downloading a sample report from any exchange you are considering. If the data is messy or incomplete, tax filing will be painful.

6. Banking relationships.

Indian banks have been hesitant to work with crypto exchanges. Good exchanges have established stable relationships with multiple banks to ensure deposit and withdrawal reliability. Check:

- Which banks does the exchange work with?

- Are deposits and withdrawals typically instant or slow?

- Any history of frozen accounts or withdrawal pauses?

Exchanges that get blacklisted by major banks become difficult to use. Your money can get stuck for days or weeks when banking relationships break down.

Warning signs on compliance:

- Exchange does not require KYC

- Exchange claims "no tax needed" or offers ways to "avoid TDS"

- Not registered with FIU-IND

- Offers Indian users features restricted in other regulated countries

- Based in jurisdictions with zero crypto regulation

- Cannot provide proper tax reports

Skipping compliance might feel convenient. It is extremely expensive long-term. The Income Tax Department receives data directly from registered Indian exchanges. If you trade on non-compliant platforms and skip tax reporting, you face penalties and interest that dwarf the tax itself.

Fees — what you actually pay

Fees eat into your returns. A trader paying 0.5% per trade vs 0.1% per trade on ₹5 lakh of monthly volume pays ₹2,000 vs ₹500 — a difference of ₹18,000 per year. Over a decade, this compounds meaningfully.

Exchange fees — every 0.1% adds up over hundreds of trades. Compare honestly.

Types of fees you will encounter:

1. Trading fees (maker/taker).

Every time you buy or sell, you pay a trading fee. Exchanges use a "maker/taker" model:

- Taker fee: You pay this when you place a market order that fills immediately (you "take" liquidity from the order book). Usually 0.1-0.25% on Indian exchanges.

- Maker fee: You pay this when you place a limit order that sits in the order book waiting to fill (you "make" liquidity). Usually 0.05-0.20% on Indian exchanges.

Some exchanges offer fee discounts for high-volume traders. Most beginners stay on basic tier rates.

2. INR deposit fees.

Most Indian exchanges offer free INR deposits through UPI and IMPS. Some charge small fees (₹2-10) for IMPS or NEFT. Direct bank transfers (RTGS) may have higher bank-side charges.

Watch out for exchanges that claim "free deposits" but charge percentages on deposit amounts. These are predatory.

3. INR withdrawal fees.

Most Indian exchanges charge small flat fees for INR withdrawals — typically ₹5-20 per withdrawal, or free above certain amounts. Some have daily withdrawal limits.

4. Crypto deposit fees.

Depositing crypto from another wallet or exchange is usually free from the receiving exchange's side. You will still pay network fees (gas fees) to the blockchain.

5. Crypto withdrawal fees.

When you withdraw crypto to an external wallet, the exchange charges a network fee. Watch for:

- Fixed fees (₹50-500 depending on the coin and network)

- Minimum withdrawal amounts (usually reasonable for beginners)

- Fee transparency — some exchanges mark up the network fee as profit

Bitcoin and Ethereum mainnet withdrawals can be expensive (₹500-2000 equivalent) during high network congestion. Layer-2 networks like Arbitrum or Optimism, and alternative chains like Polygon or BSC, have much lower fees.

6. Spread — the hidden fee.

This is the fee most beginners miss. The spread is the difference between the price at which you can buy and the price at which you can sell at any given moment.

For example, if the order book shows you can buy BTC at ₹68,50,000 but immediately sell it at ₹68,40,000, the spread is ₹10,000 (about 0.15%). You lost 0.15% just by the spread, before even paying trading fees.

Liquid exchanges with high trading volumes have tiny spreads (0.01-0.05%). Illiquid exchanges or obscure coins can have huge spreads (0.5-5%). Always check the spread before trading — multiply your total trading volume by the spread to see the real cost.

7. TDS — mandatory for Indian users.

1% TDS on every sale above ₹10,000. This is not an exchange fee but a tax. Automatic on Indian exchanges.

Total fee calculation — realistic example:

Scenario: You buy ₹50,000 of Bitcoin, then sell it a month later for ₹55,000 (₹5,000 profit).

- Buy trading fee at 0.15%: ₹75

- Buy spread at 0.05%: ₹25

- Sell trading fee at 0.15%: ₹82.50

- Sell spread at 0.05%: ₹27.50

- TDS on ₹55,000 sale: ₹550 (claimable in ITR)

- Total immediate fees: ₹210 (plus the TDS you can claim back)

On a ₹5,000 gross profit, you paid ₹210 in exchange fees (about 4.2% of gross profit). After the eventual 30% crypto tax on the profit = ₹1,560, your true net profit is about ₹3,230 — roughly 65% of gross.

This is the real math every Indian crypto trader needs to internalise. Our crypto tax guide has complete calculations. Fees plus taxes together often take 30-40% of profits. Planning for this from the start saves surprises later.

How to compare exchange fees honestly.

- List 3-4 exchanges you are considering

- Check maker and taker fees for each

- Check INR deposit and withdrawal fees

- Check typical spreads for BTC and ETH (place a small fake order to see)

- Calculate total cost for a representative trade (buy ₹10,000 of BTC, sell in 30 days)

- The lowest-cost exchange on this calculation is your winner — but security and compliance should never be compromised for fee savings

Features that matter for beginners

Beyond security, compliance, and fees, certain features make your life much easier as a beginner.

Essential features:

The exchange checklist for Indian traders — all seven should be green before you trust a single rupee.

1. Simple user interface. You should be able to place your first buy order within 30 seconds of opening the app. If the interface is confusing, you will make mistakes — clicking "sell" instead of "buy", entering wrong quantities, missing important alerts. Unnecessary complexity is dangerous for beginners.

Test this before funding any account. Download the app. Go through the entire process up to (not including) placing the order. If anything confuses you, try another exchange.

2. Multiple order types. Basic market orders are enough for most beginners. But you should have access to:

- Market order: Buy or sell immediately at current price

- Limit order: Buy or sell only if price hits your target

- Stop-loss order: Automatically sell if price drops below a threshold

- SIP (Systematic Investment Plan): Automatic recurring purchases at fixed intervals

SIP is particularly valuable for beginners who want to dollar-cost average into BTC or ETH. Not all exchanges offer it.

3. Responsive customer support.

When something goes wrong, you need help. Good exchanges offer:

- In-app chat support (ideally 24/7 for high-volume exchanges)

- Email support with response time commitments

- Detailed help documentation

- Active social media presence for urgent issues

Test support before depositing significant money. Send a question through their support channel. Note how long it takes to get a response and whether the response actually helps. This is a good preview of what a real emergency support interaction will feel like.

4. Educational resources. Exchanges like CoinDCX, Mudrex, and ZebPay offer educational content — blogs, videos, tutorials, glossaries. This is valuable for beginners, though it should never replace independent education (like what you get from cRyPtO sMaRt).

5. Coin selection.

You want at least:

- Bitcoin (BTC) — essential

- Ethereum (ETH) — essential

- Major stablecoins (USDT, USDC) — essential for portfolio rebalancing

- Top-20 coins (Solana, BNB, XRP, Cardano, etc.) — very useful

- 50-100+ altcoins — optional but gives flexibility

If an exchange does not offer top-20 coins, it is too limited for a full crypto strategy.

6. Indian-specific features.

- Prices displayed in INR (not just USD)

- Direct UPI integration for instant deposits

- Automatic TDS handling with Form 26AS integration

- Hindi or other regional language support

- Indian customer support hours and availability

7. Staking and savings products.

Some exchanges offer "earn" products where you can stake your crypto to earn yield. Rates vary widely. Approach with caution:

- Low yields (3-7% on BTC/ETH) are usually real staking and reasonably safe

- High yields (10%+ on stablecoins) are usually risky lending programs — your crypto is being lent out by the exchange

- "Too good to be true" yields (20%+ on major coins) are usually dangerous

Celsius, Voyager, and BlockFi offered similar high-yield products in 2021. All collapsed in 2022, with users losing funds. Stick to modest, transparent staking products.

Nice-to-have features:

- Price alerts (notify when your target price is hit)

- Portfolio tracker with profit/loss visualisation

- Detailed charts for technical analysis

- News and market updates integrated into the app

- Referral programs (bonus income for inviting friends)

Features to avoid (especially as a beginner):

- Margin trading: borrowing money to trade. Amplifies losses disproportionately. Our leverage trading guide explains why 90%+ of retail leveraged traders lose money.

- Futures and perpetuals: derivative contracts with complex risk. Not for beginners.

- Bots within the exchange: pre-built trading bots sold as easy money. Usually lose money or underperform simple DCA.

- Options: complex derivatives that can lose value rapidly. Master spot trading first.

Stick to simple spot buying and selling for your first 6-12 months. Advanced features tempt beginners into taking risks they do not understand.

Red flags that should make you run

A consolidated checklist of warning signs. If any exchange shows multiple of these, walk away. Your money is not worth the risk.

Immediate disqualifying red flags:

- No KYC process. If they allow trading without full identity verification, they are operating outside Indian law. Your tax exposure is your problem.

- Anonymous team. Legitimate exchanges have known founders and executives with LinkedIn profiles, interviews, media presence. Exchanges with completely anonymous teams vanish with user funds regularly.

- No physical office address. Major exchanges list their registered office address. If you cannot find one, you cannot serve legal notices or hold them accountable.

- Guaranteed returns or fixed "APY". An exchange offering "guaranteed 15% per year on your Bitcoin" is either operating a Ponzi scheme or taking on unsustainable risk that will eventually blow up.

- Unregistered with Indian authorities. FIU-IND registration and PMLA compliance are basic requirements. Non-compliant platforms will eventually be blocked or face legal action — taking your funds with them.

- No proof of reserves. After FTX, this became a baseline expectation. Exchanges that refuse to publish reserves are asking you to trust them blindly. History shows this is a bad bet.

Major red flags (multiple = avoid):

- History of hacks without proper user compensation

- Pattern of sudden withdrawal freezes or "technical issues" during market crashes

- Active regulatory action against them in any country

- Customer support non-responsive or outsourced to low-quality chatbots

- Terms of service allow them to freeze funds for vague reasons

- Recent management changes or co-founder departures (often signal internal problems)

- Heavy marketing emphasis on "easy returns" rather than security or education

- Listing extremely obscure altcoins aggressively (often paid listings, low quality)

Subtle red flags (watch for patterns):

- Website design looks hastily built or unprofessional

- Typos in legal documents, terms of service

- Social media handles are new (less than 1 year old)

- Reviews on app stores are suspiciously uniform (all 5 stars, similar language)

- "Partnerships" claimed but not verifiable from the partner's side

- Executives appear at conferences but avoid tough questions

- Celebrity endorsements without clear long-term commitment (paid shills, not real users)

Behavioural red flags during your own use:

- KYC approval is suspiciously fast (less than 30 minutes) — may indicate minimal verification

- KYC approval is suspiciously slow (more than a week) — may indicate backend problems

- Withdrawals take longer than advertised

- Small withdrawals work but larger ones get flagged

- Customer support representatives cannot answer basic technical questions

- Exchange "recommends" specific coins aggressively (often paid promotions)

- You see unexplained logins in your security history

KAVACH — Your first line of defence starts with exchange choice

KAVACH is our capital protection framework covering exchange evaluation, custody decisions (exchange vs self-custody), KYC security hygiene, and the defensive operational practices that separate traders who keep their crypto from those who lose it. Security mistakes are permanent. Learn before you trust.

Explore the Store →The diversification principle — do not put all your crypto on one exchange.

Even the best exchange can fail. History proves this. Coinbase had issues, Binance has faced regulatory attacks, WazirX had its hack. Your strategy should assume any single exchange can fail.

Practical distribution for a moderate investor:

- Active trading balance (30%): On your primary Indian exchange, ready for transactions

- Secondary holding (20%): On a second reputable Indian exchange for diversification

- Long-term holdings (50%): In a hardware wallet under your own control

This way, even a total exchange failure costs you at most 30-50% of your crypto — painful but not ruinous.

A final thought. Your exchange choice is the first real decision in your crypto journey. Take it seriously. Spend an hour reading reviews, checking registrations, testing support responsiveness. One hour of upfront work can save you lakhs of rupees in losses later. Join our Telegram community where members share real experiences (good and bad) with different Indian exchanges. Our crypto education courses include security-focused modules covering exchange selection in detail. Choose slowly. Distribute wisely. Verify continuously. That is how Indian crypto investors actually stay safe.

Frequently Asked Questions

Which is the safest crypto exchange for beginners in India in 2026?

'Safest' depends on your situation, and exchange quality can change over time. Rather than picking a single 'best' exchange, evaluate candidates on seven factors — FIU-IND registration, cold storage percentage, proof of reserves, insurance fund, KYC compliance, automatic TDS handling, and responsive customer support. Prefer Indian-headquartered exchanges for their compliance advantages. Never keep all funds on a single exchange, regardless of how safe it appears.

Can I use international crypto exchanges like Binance or Coinbase from India?

Technically yes, though regulatory requirements make Indian exchanges strongly preferable for most users. International exchanges do not automatically deduct the 1% TDS required by Indian law on crypto sales — you would be responsible for calculating and depositing TDS yourself, which is practically impossible. Also, bank transfers to fund international exchanges are sometimes flagged or frozen by Indian banks. For beginners, stick to compliant Indian exchanges.

What fees should I expect when buying crypto on an Indian exchange?

Typical Indian exchange fees: 0.10-0.25% trading fee (both buy and sell), free or near-free INR deposits via UPI/IMPS, ₹5-20 for INR withdrawals, variable crypto withdrawal fees (₹50-500 depending on network and coin), plus 1% TDS automatically deducted on sales. Watch for hidden spreads (price difference between buy and sell) which can add another 0.05-0.5%. On a ₹50,000 transaction, expect ₹150-500 in immediate fees, before the 30% crypto tax on profits.

Is it safe to store all my crypto on an Indian exchange?

No. Even the best exchanges can fail, get hacked, or face regulatory issues. A balanced approach: keep 30% of crypto on your primary exchange for active trading, 20% on a second reputable exchange for diversification, and 50% in a hardware wallet under your own control for long-term holdings. The phrase 'not your keys, not your coins' exists because exchange failures have cost users billions globally. Diversify your custody just like you diversify your investments.

What documents do I need for KYC on an Indian crypto exchange?

Standard requirements are PAN card (mandatory), Aadhaar card or other government ID, bank account linked to the same PAN, a live selfie or video verification, and proof of address (utility bill, rental agreement, or similar). Most legitimate Indian exchanges complete KYC verification in 2-24 hours. Exchanges that skip KYC entirely are operating outside Indian law — avoid them, as using them creates serious tax and legal exposure for you.

This article is for educational purposes only and does not constitute financial advice. Crypto investments are subject to market risk and are not regulated by SEBI or RBI in India. Past performance does not guarantee future results. Always do your own research, consult a registered financial advisor, and never invest more than you can afford to lose. cRyPtO sMaRt and Avik Kanrar are not liable for any trading decisions or losses based on this content.